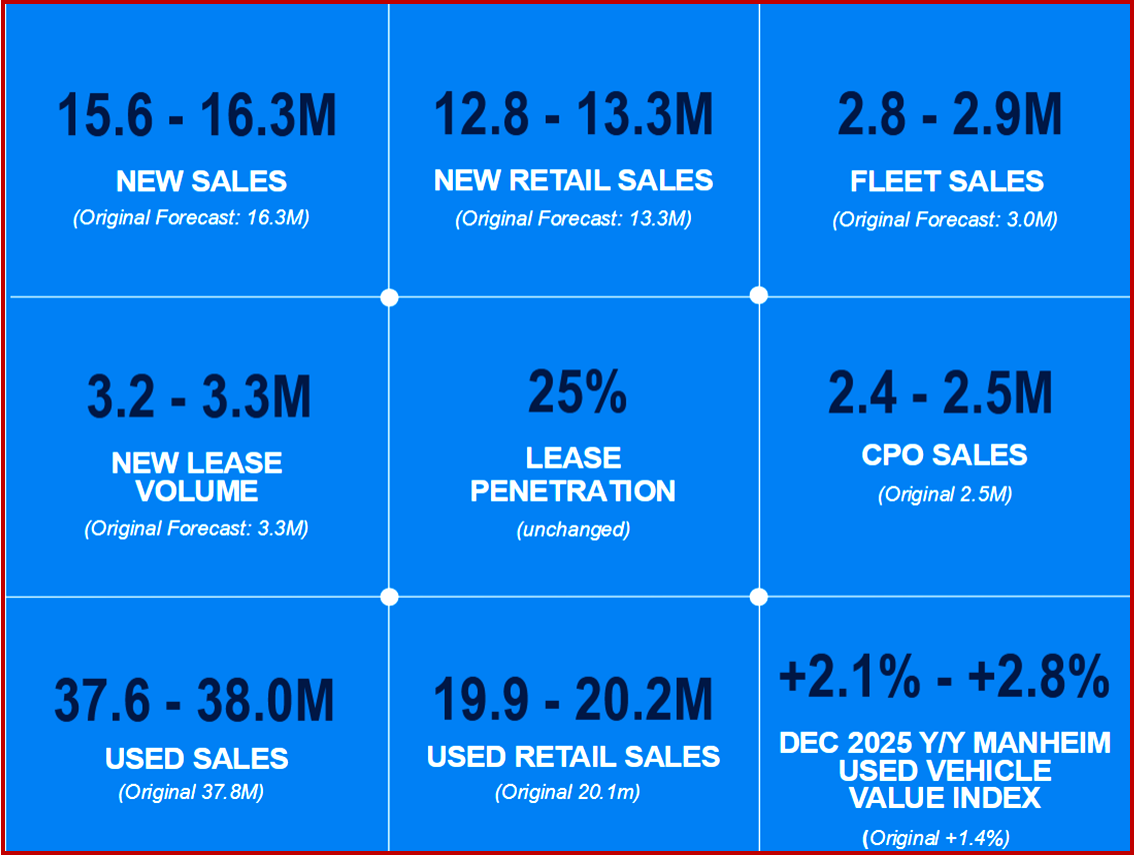

Click for more.

“The worry is that the slowing growth is getting into the territory of an engine stalled becomes more of a risk. The massive policy changes by the administration have been far more aggressive than anyone expected so far. And still the administration has communicated that they are willing to see the economy deteriorate if that is necessary to accomplish their goals. While we’re still uncertain about exact policy outcomes, it looks like we are headed for the highest active tariff rate since World War 2 for the auto market. That is especially problematic as such tariffs would be highly disruptive to North American vehicle production – resulting in tighter supply, higher prices and lower production and sales.

“The stock market is down for the year and we will likely see more declines. That produces a negative wealth effect. On spending when the economy and the vehicle market have become more dependent on higher income consumers in recent years. On top of that, rates had declined by more than a full percentage point in the fourth quarter. But have since risen more than that and reached a new 25 year high on the used average rate in February. Affordability has been holding back market potential for years, and between rates and tariffs, affordability looks to get much worse when it had looked like we had turned the corner at the end of last year.

“In addition to tariffs, the auto market also has a substantial amount of EV related policy changes that are likely to unfold later in the year. And the uncertainty from them is especially risky for manufacturers and suppliers trying to adjust their plans it. Feels like uncertainty couldn’t be higher. I’ve narrowed down the list of macro factors to the hard data points that most influenced the. Vehicle market real GDP growth is important for context, but it is the most lagging of the indicators. So it’s not going to help us until it’s much too late. ….

We are not in a recession or necessarily headed into one. But my optimism about the spring and this year has been shaken. Just think of what the spring could have been had we not been fretting about what comes next? We now know that we have higher tariffs on steel and aluminum and. all goods from China.

The most disruptive move is just one week away, as the postponed 25% tariffs on Canada and Mexico and some amount of reciprocal tariffs will go into effect on April 2nd ( a new definition of April Fool’s or Trump day – AutoCrat) on what the President is calling Liberation Day. The tariffs on Mexico and Canada are across the board with no duty drawbacks. As such, if there are no carve outs for autos and parts. They would cause a U.S. -made vehicle to add $3000 in cost and likely $6000 or more on a typical vehicle assembled in Canada or Mexico. If the tariffs go through this time by mid-April, we expect disruption to virtually all North American vehicle production amounting to 20,000 fewer vehicles produced per day. Which is about a 30% hit to production over the longer term. We expect sales of fall, new and used prices to increase and some models to be eliminated. If those tariffs persist – and we’ve yet to hear details about tariffs on the European Union, Japan and South Korea. Just this Monday, the President suggested we’d hear more about auto tariffs before liberation. OK. Bottom Line: lower production, tighter supply and higher prices are around the corner. Reminiscent of 2021, uncertainty could make it even worse. Half of the affordable vehicles sold in the US are dependent on Mexico and Canada. With added cost, those nameplates will likely be eliminated. The way this is done also is not conducive to demand increases. Ahead of the change, it’s just been unseen and chaotic. We still don’t know details and we’re days away. Buyers will try and wait for them to go away, but will they go away? On that note, I’ll go take some blood pressure medication.