Click for more GlobalData.

Global Data Observations and Opinions

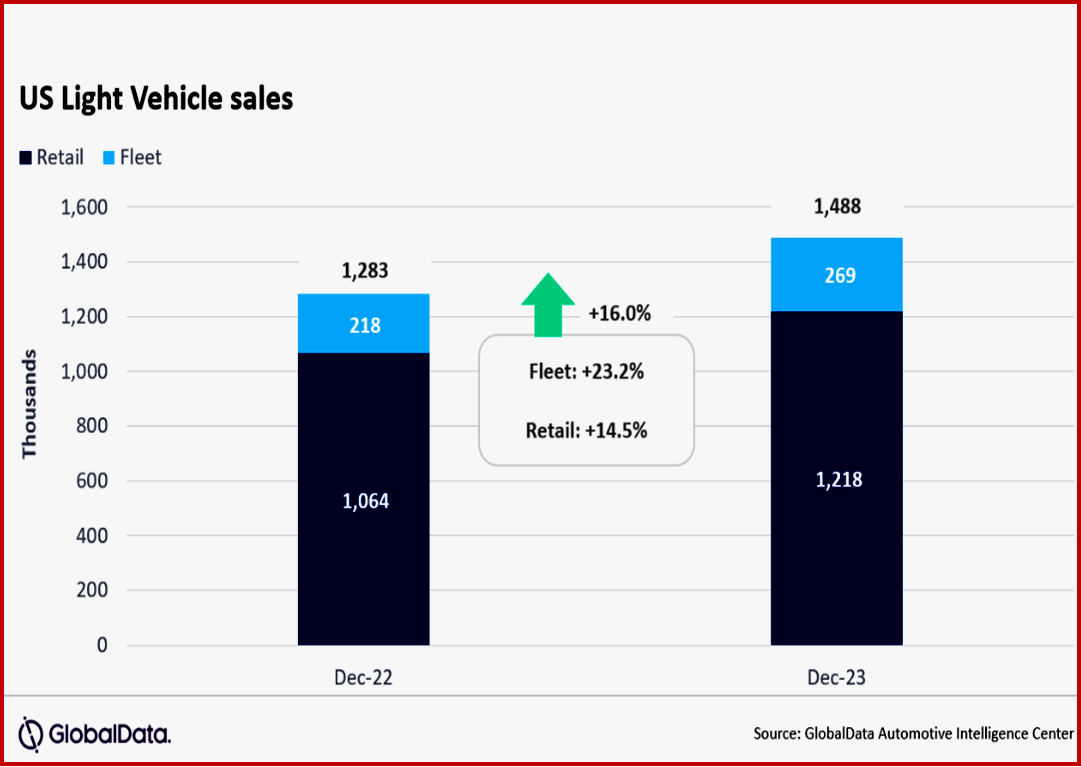

• General Motors returned to the top of the sales rankings with 234,000units, finishing ~8000 units ahead of Toyota Group after the Japanese OEM led the market in the previous two months.

• Ford Group was in third on 186,000 units and, at 12.5%, its market share was the highest since July.

• Toyota brand led at 188,000 units, ahead of Ford at 176,000 units.

• Ford was only marginally ahead of Chevrolet in November, in December the difference widened to 23,000 units.

• Toyota RAV4 was the bestselling model at 47,000 units for a third consecutive month, but the gap to the Ford F-150 was smaller than in November, at 3000. RAV4 appears to have continued to benefit from an abnormally high level of imports, but this is understood to be a temporary situation.

• Compact Non-Premium SUV was comfortably the leading segment once again, although its market share eased slightly from November levels to 20.7%. Mid-size Non-Premium SUV saw its highest share since May at 16.2%, followed by Large Pickup at 13.6%.

“While one month’s results should not be interpreted as necessarily heralding a return to previous highs, consumers in December showed a willingness to purchase if the price was right. Continued discounting or moderating pricing could bring a more pronounced lift to demand in 2024. That said, we expect a slight January hangover in demand, given the likely pull forward, and there remains economic risk that needs to be factored in as we start the new year. The overall state of the economy and pricing trends will be the dominant drivers in auto demand for 2024,” said Jeff Schuster, Vice President Research and Analysis, Automotive.