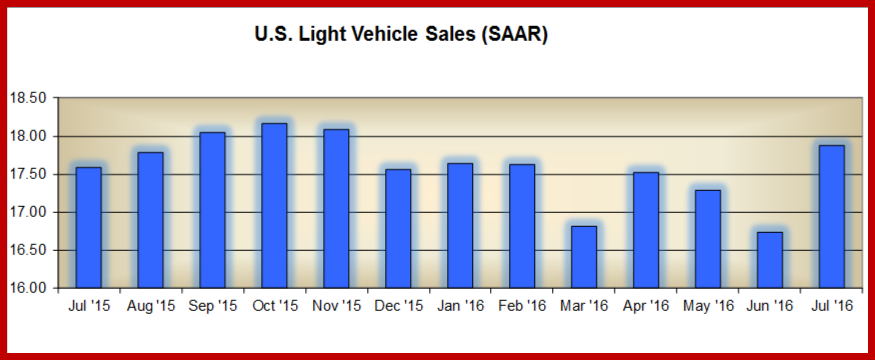

U.S. auto lease ABS residual performance is still producing gains overall through mid-summer despite rising used vehicle supplies, Fitch Ratings says. However, further increases in vehicle supply in second-half 2016 and into 2017 could lead to pressure on residual values (RV).

Fitch’s quarterly RV ABS index slowly declined over the past year. The index recorded a RV gain of 2.51% as of second-quarter 2016, down from 4.79% in second-quarter 2015 and 8.39% at second-quarter 2014. The average yearly gain in 2014 was 5.75%, which then slowed to 3.97% in 2015, and averaged 2.10% for the first half of 2016. The peak RV gain was 29.21% observed in first-quarter 2011. Fitch’s outlook for auto lease ABS asset performance remains stable for the second half of 2016. This is supported by continual growing credit enhancement levels resulting in healthy levels of loss protection.

The persistent RV gains, albeit at a lower level, are partially due to the conservative establishment of securitized residuals in US auto lease transactions. Securitized residuals in US. auto lease ABS are often defined as the lesser of residual value established by the servicer at lease inception, Automotive Lease Guide’s (ALG) value at inception, or ALG’s mark-to-market value at the time of the transaction’s closing. By securitizing the lowest of these and comparing that value to lease-end sales prices in determining an RV loss or gain, there is built-in RV loss protection.

Fitch expects the pace of upgrades to subordinate notes to continue for auto lease ABS in the second half of 2016. Upgrades are driven in large part to delivering transaction structures and growing credit enhancement levels. Further, Fitch’s base case or ‘BBsf’ RV loss proxy is conservatively determined by isolating only the RV losses an issuer observed during the worst 12-18 month period, typically during the weakest 2008-2009 period.

U.S. auto lease ABS residual performance is still producing gains overall through mid-summer despite rising used vehicle supplies, Fitch Ratings says. However, further increases in vehicle supply in second-half 2016 and into 2017 could lead to pressure on residual values (RV).

Fitch’s quarterly RV ABS index slowly declined over the past year. The index recorded a RV gain of 2.51% as of second-quarter 2016, down from 4.79% in second-quarter 2015 and 8.39% at second-quarter 2014. The average yearly gain in 2014 was 5.75%, which then slowed to 3.97% in 2015, and averaged 2.10% for the first half of 2016. The peak RV gain was 29.21% observed in first-quarter 2011. Fitch’s outlook for auto lease ABS asset performance remains stable for the second half of 2016. This is supported by continual growing credit enhancement levels resulting in healthy levels of loss protection.

The persistent RV gains, albeit at a lower level, are partially due to the conservative establishment of securitized residuals in US auto lease transactions. Securitized residuals in US. auto lease ABS are often defined as the lesser of residual value established by the servicer at lease inception, Automotive Lease Guide’s (ALG) value at inception, or ALG’s mark-to-market value at the time of the transaction’s closing. By securitizing the lowest of these and comparing that value to lease-end sales prices in determining an RV loss or gain, there is built-in RV loss protection.

Fitch expects the pace of upgrades to subordinate notes to continue for auto lease ABS in the second half of 2016. Upgrades are driven in large part to delivering transaction structures and growing credit enhancement levels. Further, Fitch’s base case or ‘BBsf’ RV loss proxy is conservatively determined by isolating only the RV losses an issuer observed during the worst 12-18 month period, typically during the weakest 2008-2009 period.