Click to Enlarge

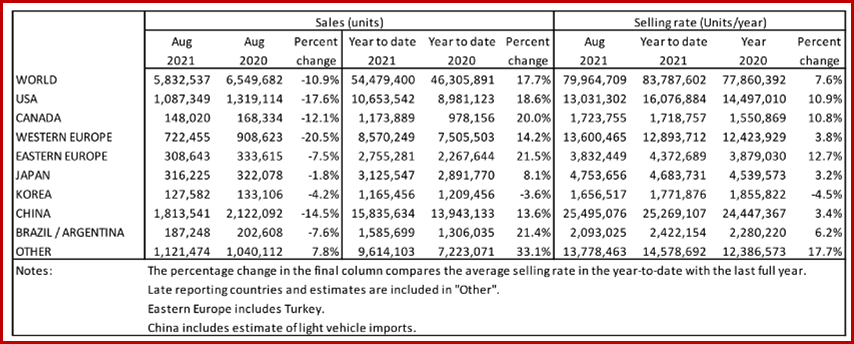

The Global Light Vehicle (LV) selling rate was 82 mn units/year in July, prolonging the weaker trend seen in recent months. The semiconductor shortage held back the post-lockdown recovery of vehicle sales in Europe, while its impact on inventories in the US meant average transaction prices rocketed, according to the LMC Automotive Consultancy. Worse, rising Delta variant cases threaten to impair the outlook in parts of Asia.

The US Light Vehicle market continued to be hurt by low inventories during July. Sales grew by only 3.2% YoY, to 1.28 mn units. This is a slight advance compared to July 2020’s pandemic-affected result. The selling rate declined more to 14.6 mn units/year, from 15.4 mn units/year in June. This is the lowest rate since June 2020.

The inequality of supply and demand resulted in average US transaction prices of $40,879 in July, the first time ever been above $40,000. This disaster for consumers was good for automakers. Incentives fell to a record low of just 4.6% of MSRP, or $1968 per unit. The semiconductor shortage will drop GM’s wholesale deliveries by about 200,000 vehicles in North America during the second half of the year compared to the 1.1 million it delivered in the first half of the year, GM said on Friday.

Canada LV sales fell by 2.2% YoY in July, to 156k units. This was the first YoY decline since February, while the selling rate decreased to 1.6 mn units/year in July, from 1.73 mn units/year in June, says LMC. Although the COVID-19 plague has improved in Canada, the industry is now being significantly affected by inventory shortages. Mexican LV sales were up by 12.6% YoY in July, to 82k units, but the selling rate fell for a third consecutive month, to 994k units/year, from 1.07 mn units/year in June.

The West European selling rate dropped to 12.3 mn units/year in July, from 13.7 mn units/year in June. The supply-side issue of the availability of semiconductor chips is “clearly having a negative impact on selling rate recovery in the region, holding back the post-lockdown rebound in demand,” said LMC.

The Eastern Europe selling rate fell to 4.0 mn units/year in July, from 4.5 mn units/year in June. In Russia, the selling rate “was likely held back by the semiconductor shortage, while Poland’s selling rate has recently seen an improvement to 500k units/year, because of a sustained fall in COVID-19 cases.

LMC notes that advance data indicates that the Chinese market regained momentum in July. The July selling rate reached 27.9 mn units/year, up 10% from a weak June, and was the highest rate since December 2020. In the first seven months of this year, the selling rate averaged 25.2 mn units/year, which is above the 2020 result of 24.4 mn units, but still a touch below the 2019 sales of 25.5 mn units. In YoY terms, sales declined by nearly 10% in July, but increased by 19% YTD, due to distortions caused by the pandemic.

During July, NEV sales stimulated the market, expanding by a robust 180% YoY. Most global brands suffered YoY declines due to the supply issue from the global chip shortage, while Chinese brands, such as GAC Motor, Great Wall and Changan, continued to perform well. “Looking ahead, the fast spread of the Delta variant across the country and tightened social restrictions present a risk to economic activity and new vehicle sales,” said LMC.

The Japanese July selling rate was 4.17 mn units/year, up slightly from June, but that was the second lowest rate in a year. The chip shortage and supply-chain disruptions – from the spread of the virus in other parts of Asia – led to supply constraints. In addition, the skyrocketing number of COVID-19 infections hurt consumer confidence. The selling rate averaged 4.7 mn units/year YTD, compared to the 2019 result of 5.1 mn units.

Preliminary data indicates that Korea’s selling rate slowed to 1.66 mn units/year in July, down nearly 7% from June. The chip condition has improved, but supply was disrupted by Hyundai’s temporarily halt in production at its Asan plant to prepare the facility for BEV production. “The soaring number of COVID-19 cases and the strict social distancing measures in the Greater Seoul area undermined sales, too.,” said LMC.

Brazilian LV sales fell by 0.5% YoY in July, to 163k units. This is the first YoY contraction since February, when the year-ago month was unaffected by the pandemic. The weak market was underlined by the fact that the selling rate fell to 1.77 mn units/year in July, from 1.97 mn units/year in June. July’s rate was the lowest since June 2020. Production lines for some key models remain down amid the chip shortage, inventory of those models has virtually run out, “decimating sales.”

In Argentina, LV sales grew by 5.3% YoY in July, to 30k units. The selling rate declined to 345k units/year in July, from 399k units/year in June. July’s selling rate “would appear to represent a fairer picture of the current state of the market,” according to LMC.

AutoInformed.com on

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

August Global Light Vehicle Sales Weaken Again

Click to Enlarge

The Global Light Vehicle (LV) selling rate was 82 mn units/year in July, prolonging the weaker trend seen in recent months. The semiconductor shortage held back the post-lockdown recovery of vehicle sales in Europe, while its impact on inventories in the US meant average transaction prices rocketed, according to the LMC Automotive Consultancy. Worse, rising Delta variant cases threaten to impair the outlook in parts of Asia.

The US Light Vehicle market continued to be hurt by low inventories during July. Sales grew by only 3.2% YoY, to 1.28 mn units. This is a slight advance compared to July 2020’s pandemic-affected result. The selling rate declined more to 14.6 mn units/year, from 15.4 mn units/year in June. This is the lowest rate since June 2020.

The inequality of supply and demand resulted in average US transaction prices of $40,879 in July, the first time ever been above $40,000. This disaster for consumers was good for automakers. Incentives fell to a record low of just 4.6% of MSRP, or $1968 per unit. The semiconductor shortage will drop GM’s wholesale deliveries by about 200,000 vehicles in North America during the second half of the year compared to the 1.1 million it delivered in the first half of the year, GM said on Friday.

Canada LV sales fell by 2.2% YoY in July, to 156k units. This was the first YoY decline since February, while the selling rate decreased to 1.6 mn units/year in July, from 1.73 mn units/year in June, says LMC. Although the COVID-19 plague has improved in Canada, the industry is now being significantly affected by inventory shortages. Mexican LV sales were up by 12.6% YoY in July, to 82k units, but the selling rate fell for a third consecutive month, to 994k units/year, from 1.07 mn units/year in June.

The West European selling rate dropped to 12.3 mn units/year in July, from 13.7 mn units/year in June. The supply-side issue of the availability of semiconductor chips is “clearly having a negative impact on selling rate recovery in the region, holding back the post-lockdown rebound in demand,” said LMC.

The Eastern Europe selling rate fell to 4.0 mn units/year in July, from 4.5 mn units/year in June. In Russia, the selling rate “was likely held back by the semiconductor shortage, while Poland’s selling rate has recently seen an improvement to 500k units/year, because of a sustained fall in COVID-19 cases.

LMC notes that advance data indicates that the Chinese market regained momentum in July. The July selling rate reached 27.9 mn units/year, up 10% from a weak June, and was the highest rate since December 2020. In the first seven months of this year, the selling rate averaged 25.2 mn units/year, which is above the 2020 result of 24.4 mn units, but still a touch below the 2019 sales of 25.5 mn units. In YoY terms, sales declined by nearly 10% in July, but increased by 19% YTD, due to distortions caused by the pandemic.

During July, NEV sales stimulated the market, expanding by a robust 180% YoY. Most global brands suffered YoY declines due to the supply issue from the global chip shortage, while Chinese brands, such as GAC Motor, Great Wall and Changan, continued to perform well. “Looking ahead, the fast spread of the Delta variant across the country and tightened social restrictions present a risk to economic activity and new vehicle sales,” said LMC.

The Japanese July selling rate was 4.17 mn units/year, up slightly from June, but that was the second lowest rate in a year. The chip shortage and supply-chain disruptions – from the spread of the virus in other parts of Asia – led to supply constraints. In addition, the skyrocketing number of COVID-19 infections hurt consumer confidence. The selling rate averaged 4.7 mn units/year YTD, compared to the 2019 result of 5.1 mn units.

Preliminary data indicates that Korea’s selling rate slowed to 1.66 mn units/year in July, down nearly 7% from June. The chip condition has improved, but supply was disrupted by Hyundai’s temporarily halt in production at its Asan plant to prepare the facility for BEV production. “The soaring number of COVID-19 cases and the strict social distancing measures in the Greater Seoul area undermined sales, too.,” said LMC.

Brazilian LV sales fell by 0.5% YoY in July, to 163k units. This is the first YoY contraction since February, when the year-ago month was unaffected by the pandemic. The weak market was underlined by the fact that the selling rate fell to 1.77 mn units/year in July, from 1.97 mn units/year in June. July’s rate was the lowest since June 2020. Production lines for some key models remain down amid the chip shortage, inventory of those models has virtually run out, “decimating sales.”

In Argentina, LV sales grew by 5.3% YoY in July, to 30k units. The selling rate declined to 345k units/year in July, from 399k units/year in June. July’s selling rate “would appear to represent a fairer picture of the current state of the market,” according to LMC.

AutoInformed.com on

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.