Click to enlarge.

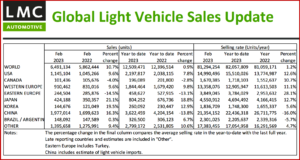

The Global Light Vehicle selling rate in February fell to 81 million units a year from January’s 83 million, according to the latest data just released by LMC Automotive*. “While global supply-side constraints remain a drag on the sector’s recovery, raw monthly registrations increased to 6.5 million – growth of almost 11% year-on-year, LMC said. (autoinformed.com on: January Global Light Vehicle Sales Flat at 83 Million)

The drop in SAAR, seasonally adjusted annual rate, is from a slow down in the Chinese market, affected by the Chinese New Year and termination of tax incentives in 2022. Both North America and Western Europe saw YoY improvements in performance when compared against a weak 2022,. Eastern Europe continues to suffer YoY negative growth.

North America

US LV sales grew by 9.6% YoY in February, to 1.1 million units. While the selling rate slowed to 15.0 million units/year, from 16.0 million units/year in January, the persistent supply‐side issues have disrupted seasonality, making the selling rate a weak indicator of the market’s strength. February sales surpassed expectations, despite high average transaction prices at US$46,015, up by 4.3% YoY. Incentives are starting to increase modestly, at US$1,415 last month (+11.0% YoY).

Canadian LV sales fell 4.0% YoY, at 101,000, with the selling rate estimated to have declined to 1.7 million units/year in February, from 1.8 million units/year in January. LMC said improved inventory levels are likely to support sales activity this year. In Mexico, sales increased by 28.4% YoY in February to around 102k units. The selling rate accelerated to 1.4 million units/year, from 1.2 million units/year in January.

Europe

The West European selling rate rose from 12.5 million units/year in January to 13.4 million units/year in February. In preliminary raw monthly terms, February registered 910k units, up 9.6% YoY. “However, this is in comparison to a weak February 2022,” LMC noted.

The East European selling rate also picked up from January to February. The Ukraine war is still hinders the LV market in the region, with preliminary raw registrations at 240,000 units, down 14.5% YoY. This fall is led by Putin’s Russia, where raw registrations fell by~60% YoY.

China

Preliminary February data in the opaque Chinese market show that, as expected, it decelerated further. The February selling rate was 21.4 million units/year, down 9% from a lazy January, and the lowest rate since the Shanghai lock-down in April 2022. “In YoY terms, however, sales increased by 16% against a low base, due to the timing of the Chinese New Year. Weak sales in January and February can be attributed to the fact that two major tax incentives for both Internal Combustion Engine, ICE, and New Electric Vehicle, NEV, models were terminated at the end of last year,” LMC said.

“With sales are slumping, automakers are now cutting prices and provincial governments are rushing to offer subsidies – primarily for new vehicles that are assembled in their own province. Following the big price cuts by Tesla, the price war has spread beyond EVs to ICE models. “That should help boost sales in the coming months, as most economic activities have returned to normal after the pandemic subsided,” LMC said.

Elsewhere in Asia

In Japan, the selling rate slowed to 4.6 million units/year in February but averaged 4.7 million units/year in the first two months of this year. Thanks to an easing of global supply bottlenecks, OEMs ramped up production and thus increased deliveries. “Yet, the semiconductor shortage is far from over, continuing to disrupt production. The waiting periods for most models remain long, ranging from a few months to a few years,” LMC said.

In Korea, the February selling rate reached a near two‐year high of 1.8 million units/year, up 11% from a month ago. Sales were aided by the tax incentives for Passenger Vehicles (PVs) and the recently launched 2023 BEV subsidy program. The new scheme provides BEV sales with various cash subsidies, based on vehicle price, vehicle performance, after‐sales service infrastructure, and battery energy density, and will likely give Hyundai and Kia an advantage over imported brands, such as Tesla and Mercedes.

South America

Brazilian LV sales fell by 0.8% YoY in February, to 120k units. The selling rate accelerated to 1.9 million units/year, from 1.7 million units/year in January but his was still a weak outcome. In volume, it was the weakest February since 2005, but there were two fewer selling days than last year, while the annual Carnival celebrations could have impacted sales to some extent. While inventory continues to improve (187,000 units in February) affordability is still a concern as prices rise and consumers face economic uncertainty. LMC observed.

In Argentina, sales are estimated to have increased by 5.6% YoY in February, to 28.3k units, while the selling rate accelerated to 394k units/year, from 375k units/year in January. The result was close to the previous six months’ average selling rate, as the market continues to tick over, albeit at a much lower level than in previous years, with economic headwinds and import restrictions keeping sales flat.

*LMC Automotive – a GlobalData Company

LMC Automotive is a leading independent and exclusively automotive focused provider of global forecasting and market intelligence in the areas of vehicle sales, production, powertrains and electrification. The company’s global clients include car and truck makers, component manufacturers and suppliers, financial, logistics and government institutions. LMC Automotive is part of the LMC group, as is J.D. Power. LMC is also the world’s leading economic and business consultancy for the agribusiness sector.

The Global Light Vehicle Sales Forecast. Published in association with Jato Dynamics Ltd, builds on macro‐economic forecasts generated by our partner, the renowned Oxford Economics, which, combined with an examination of demographics, fiscal and regulatory influences by LMC’s own specialist automotive research team, presents twelve‐year forecasts at a global, regional and country level for Light Vehicle demand in 137 countries.

In its most detailed form, model level forecasts are updated monthly and are provided in annual, quarterly and monthly time slices. Quarterly summary reports analyze the current market situation and likely future evolution from the perspective of developments at a country level and from the position of each major OEM. For more information about LMC Automotive, visit www.lmc-auto.com. or contact LMC directly at forecasting@lmc-auto.com.

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

February Global Light Vehicle Sales Up 11% at 6.5 Million

Click to enlarge.

The Global Light Vehicle selling rate in February fell to 81 million units a year from January’s 83 million, according to the latest data just released by LMC Automotive*. “While global supply-side constraints remain a drag on the sector’s recovery, raw monthly registrations increased to 6.5 million – growth of almost 11% year-on-year, LMC said. (autoinformed.com on: January Global Light Vehicle Sales Flat at 83 Million)

The drop in SAAR, seasonally adjusted annual rate, is from a slow down in the Chinese market, affected by the Chinese New Year and termination of tax incentives in 2022. Both North America and Western Europe saw YoY improvements in performance when compared against a weak 2022,. Eastern Europe continues to suffer YoY negative growth.

North America

US LV sales grew by 9.6% YoY in February, to 1.1 million units. While the selling rate slowed to 15.0 million units/year, from 16.0 million units/year in January, the persistent supply‐side issues have disrupted seasonality, making the selling rate a weak indicator of the market’s strength. February sales surpassed expectations, despite high average transaction prices at US$46,015, up by 4.3% YoY. Incentives are starting to increase modestly, at US$1,415 last month (+11.0% YoY).

Canadian LV sales fell 4.0% YoY, at 101,000, with the selling rate estimated to have declined to 1.7 million units/year in February, from 1.8 million units/year in January. LMC said improved inventory levels are likely to support sales activity this year. In Mexico, sales increased by 28.4% YoY in February to around 102k units. The selling rate accelerated to 1.4 million units/year, from 1.2 million units/year in January.

Europe

The West European selling rate rose from 12.5 million units/year in January to 13.4 million units/year in February. In preliminary raw monthly terms, February registered 910k units, up 9.6% YoY. “However, this is in comparison to a weak February 2022,” LMC noted.

The East European selling rate also picked up from January to February. The Ukraine war is still hinders the LV market in the region, with preliminary raw registrations at 240,000 units, down 14.5% YoY. This fall is led by Putin’s Russia, where raw registrations fell by~60% YoY.

China

Preliminary February data in the opaque Chinese market show that, as expected, it decelerated further. The February selling rate was 21.4 million units/year, down 9% from a lazy January, and the lowest rate since the Shanghai lock-down in April 2022. “In YoY terms, however, sales increased by 16% against a low base, due to the timing of the Chinese New Year. Weak sales in January and February can be attributed to the fact that two major tax incentives for both Internal Combustion Engine, ICE, and New Electric Vehicle, NEV, models were terminated at the end of last year,” LMC said.

“With sales are slumping, automakers are now cutting prices and provincial governments are rushing to offer subsidies – primarily for new vehicles that are assembled in their own province. Following the big price cuts by Tesla, the price war has spread beyond EVs to ICE models. “That should help boost sales in the coming months, as most economic activities have returned to normal after the pandemic subsided,” LMC said.

Elsewhere in Asia

In Japan, the selling rate slowed to 4.6 million units/year in February but averaged 4.7 million units/year in the first two months of this year. Thanks to an easing of global supply bottlenecks, OEMs ramped up production and thus increased deliveries. “Yet, the semiconductor shortage is far from over, continuing to disrupt production. The waiting periods for most models remain long, ranging from a few months to a few years,” LMC said.

In Korea, the February selling rate reached a near two‐year high of 1.8 million units/year, up 11% from a month ago. Sales were aided by the tax incentives for Passenger Vehicles (PVs) and the recently launched 2023 BEV subsidy program. The new scheme provides BEV sales with various cash subsidies, based on vehicle price, vehicle performance, after‐sales service infrastructure, and battery energy density, and will likely give Hyundai and Kia an advantage over imported brands, such as Tesla and Mercedes.

South America

Brazilian LV sales fell by 0.8% YoY in February, to 120k units. The selling rate accelerated to 1.9 million units/year, from 1.7 million units/year in January but his was still a weak outcome. In volume, it was the weakest February since 2005, but there were two fewer selling days than last year, while the annual Carnival celebrations could have impacted sales to some extent. While inventory continues to improve (187,000 units in February) affordability is still a concern as prices rise and consumers face economic uncertainty. LMC observed.

In Argentina, sales are estimated to have increased by 5.6% YoY in February, to 28.3k units, while the selling rate accelerated to 394k units/year, from 375k units/year in January. The result was close to the previous six months’ average selling rate, as the market continues to tick over, albeit at a much lower level than in previous years, with economic headwinds and import restrictions keeping sales flat.

*LMC Automotive – a GlobalData Company

LMC Automotive is a leading independent and exclusively automotive focused provider of global forecasting and market intelligence in the areas of vehicle sales, production, powertrains and electrification. The company’s global clients include car and truck makers, component manufacturers and suppliers, financial, logistics and government institutions. LMC Automotive is part of the LMC group, as is J.D. Power. LMC is also the world’s leading economic and business consultancy for the agribusiness sector.

The Global Light Vehicle Sales Forecast. Published in association with Jato Dynamics Ltd, builds on macro‐economic forecasts generated by our partner, the renowned Oxford Economics, which, combined with an examination of demographics, fiscal and regulatory influences by LMC’s own specialist automotive research team, presents twelve‐year forecasts at a global, regional and country level for Light Vehicle demand in 137 countries.

In its most detailed form, model level forecasts are updated monthly and are provided in annual, quarterly and monthly time slices. Quarterly summary reports analyze the current market situation and likely future evolution from the perspective of developments at a country level and from the position of each major OEM. For more information about LMC Automotive, visit www.lmc-auto.com. or contact LMC directly at forecasting@lmc-auto.com.

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.