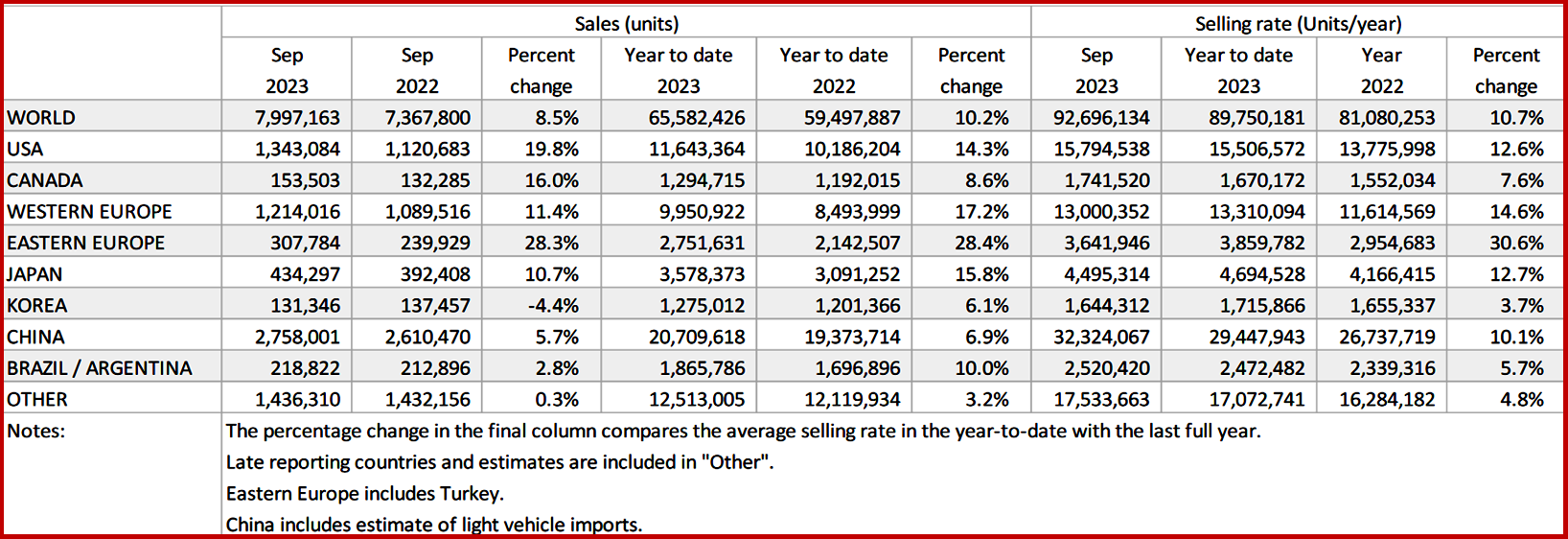

The Global Light Vehicle (LV) selling rate ended its 6-month rising streak by falling to 93 million units/year in September, from a revised figure of 100 million units in August, according to data just released by the respected consultancy GlobalData.* With 8 million units sold in September, the global LV market has grown 8.5% Year-over-Year (YoY). Year-to-date (YTD), there have been 66 million units sold, posting an increase of 10.2% YoY. (AutoInformed: August Global Light Vehicle Sales Up Again)

The US, Western and Eastern European countries all had double digit YoY growth, partly due to the COVID plague year of 2022 being a weak base and also because of an alleviation in supply-side issues. Chinese sales grew 5.7%, helped by a booming export sector, while the domestic market was helped by personal income tax cuts and price reductions across automakers, according to GlobalData Light Vehicle Sales Forecasting Team.

Click for more GlobalData.

GlobalData Observations and Commentary

North America

The US Light Vehicle market displayed another strong month in September, as vehicle sales reached1.3 million units, increasing by 19.8% YoY. The selling rate increased significantly in September to 15.8 million units/year, up from a revised figure of 15.4 million units/year reported in August. “There was no discernible impact from the UAW strikes in September, as OEMs had sufficient inventory to meet demand. Transaction prices remain at an elevated level, but in September the average price dropped by US$171 Month-over-Month (MoM) to US $45,764. Incentives also slightly dropped in September, to US $1,838, down by US $66 MoM, this could be due to OEMs reducing incentive spend as they monitor potential strike outcomes.”

Canadian Light Vehicles September sales reached 153,500 units, an increase of 16.0% YoY. The selling rate also increased in September, to 1.74 million units/year, compared to a revised figure of 1.68 million units/year reported in August. “The Canadian market also performed better than previously thought in Q3 overall.”

Mexican sales increased by 38.0% YoY, to 117,900 units in September. The selling rate increased in September, to 1.48 million units/year, “the highest the rate has been since September 2018.”

Europe

The Western Europe LV selling rate slowed to 13 million units/year in September from an upwards adjusted 16.5 million units/year in August, registering 1.2 million vehicles (+11.4% YoY). “The region’s YoY growth continues to be the result of an improved supply of components and higher delivery rates.” Year-to-date (YTD), the region has grown 17.2% YoY with total sales of 9.95 million units.

The East European LV selling rate rose to 3.6 million units/year in September, following a MoM increase in the raw monthly registration figure of 308,000 units (28.3% YoY). “The strong YoY growth was supported by Russia selling more than 84,000 units in September, which is 56% higher than the same period last year. While the YTD figure for the region (2.8 million units) is up 28.4% YoY, it is still down 7% from pre-pandemic 2019 levels.”

China

According to preliminary data, sales in China (wholesales that include exports) maintained a robust pace. “Although the September selling rate of 32.3 million units/year was 10% lower than the abnormally strong August, that was a very high level.” The YTD selling rate averaged 29.4 million units/year, exceeding last year’s total Light Vehicle sales of 26.7 million units. In YoY terms, sales expanded by 5.7% in September and nearly 7% YTD.

As has been the case in the recent months, booming exports (especially of New Electric Vehicles, aka NEVs) led wholesales in September. Domestic sales fared well, too.” Domestic sales of Passenger Vehicles were flat (+0%)YoY, but that was still a good result, as sales a year ago were high due to the post-lock-down rebound. In August, Tesla initiated a new round of price cuts, which triggered a wave of massive price reductions among other major automakers. That, along with the recent personal income tax cut, helped sales.”

Elsewhere in Asia

In Japan, sales remain buoyant, but the selling rate slowed to a more sustainable level of 4.5 million units/year in September, after spiking to an exceptionally high 5.4 million units/year in August. Supply continued to catch up, boosting sales. Yet, there are signs that demand is now slowing, in the face of high inflation and falling real wages. Inflation-adjusted real wages fell for the 17th consecutive month in August, impacting consumers’ purchasing power.

The Korean market has started to lose momentum, hit by tighter credit conditions and a slowing economy, as well as the expiry of the temporary excise tax cut in June. The September selling rate was 1.64 million units/year, not a bad result, but lackluster. All Korean brands, except Kia, reported a YoY decline in sales in September, although that was due partially to a high base. Sales of Light Commercial Vehicles were particularly weak. BEV sales also failed to sustain strong growth.

South America

Preliminary estimates indicate that Brazilian Light Vehicle sales increased by 3.8% YoY in September, to 187,400. As sales have increased YoY, the selling rate also increased to 2.17 million units/year, up from 2.14 million units/year reported in August. Sales for the country have been slowly declining since peaking at 215, 500 in July, as demand has cooled after the end of the government incentive scheme. Falling sales could also account for the increase in inventory, as the quantity of vehicles in stock grew to 265,800 units in September, up from 244,700 units in August.

In Argentina, Light Vehicle sales are estimated to have decreased by 2.9% YoY in September, to 31,400. LV sales suffered a slowdown on a MoM basis, and the selling rate also declined to 347,000 a year, down from 398,000 units/year in August. This is the lowest the selling rate has been since September 2022. There was a sharp drop in sales of imported models in September, accounting for little more than 20% of total volumes, which likely caused the weak overall performance.

*GlobalData

GlobalData says that “4000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, financial, technology and professional services sectors.” J.D. Power is also part of GlobalData. Inquiries at: customersuccess.automotive@globaldata.com.

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

September Global Light Vehicle Sales Grow But Rate Slows

The Global Light Vehicle (LV) selling rate ended its 6-month rising streak by falling to 93 million units/year in September, from a revised figure of 100 million units in August, according to data just released by the respected consultancy GlobalData.* With 8 million units sold in September, the global LV market has grown 8.5% Year-over-Year (YoY). Year-to-date (YTD), there have been 66 million units sold, posting an increase of 10.2% YoY. (AutoInformed: August Global Light Vehicle Sales Up Again)

The US, Western and Eastern European countries all had double digit YoY growth, partly due to the COVID plague year of 2022 being a weak base and also because of an alleviation in supply-side issues. Chinese sales grew 5.7%, helped by a booming export sector, while the domestic market was helped by personal income tax cuts and price reductions across automakers, according to GlobalData Light Vehicle Sales Forecasting Team.

Click for more GlobalData.

GlobalData Observations and Commentary

North America

The US Light Vehicle market displayed another strong month in September, as vehicle sales reached1.3 million units, increasing by 19.8% YoY. The selling rate increased significantly in September to 15.8 million units/year, up from a revised figure of 15.4 million units/year reported in August. “There was no discernible impact from the UAW strikes in September, as OEMs had sufficient inventory to meet demand. Transaction prices remain at an elevated level, but in September the average price dropped by US$171 Month-over-Month (MoM) to US $45,764. Incentives also slightly dropped in September, to US $1,838, down by US $66 MoM, this could be due to OEMs reducing incentive spend as they monitor potential strike outcomes.”

Canadian Light Vehicles September sales reached 153,500 units, an increase of 16.0% YoY. The selling rate also increased in September, to 1.74 million units/year, compared to a revised figure of 1.68 million units/year reported in August. “The Canadian market also performed better than previously thought in Q3 overall.”

Mexican sales increased by 38.0% YoY, to 117,900 units in September. The selling rate increased in September, to 1.48 million units/year, “the highest the rate has been since September 2018.”

Europe

The Western Europe LV selling rate slowed to 13 million units/year in September from an upwards adjusted 16.5 million units/year in August, registering 1.2 million vehicles (+11.4% YoY). “The region’s YoY growth continues to be the result of an improved supply of components and higher delivery rates.” Year-to-date (YTD), the region has grown 17.2% YoY with total sales of 9.95 million units.

The East European LV selling rate rose to 3.6 million units/year in September, following a MoM increase in the raw monthly registration figure of 308,000 units (28.3% YoY). “The strong YoY growth was supported by Russia selling more than 84,000 units in September, which is 56% higher than the same period last year. While the YTD figure for the region (2.8 million units) is up 28.4% YoY, it is still down 7% from pre-pandemic 2019 levels.”

China

According to preliminary data, sales in China (wholesales that include exports) maintained a robust pace. “Although the September selling rate of 32.3 million units/year was 10% lower than the abnormally strong August, that was a very high level.” The YTD selling rate averaged 29.4 million units/year, exceeding last year’s total Light Vehicle sales of 26.7 million units. In YoY terms, sales expanded by 5.7% in September and nearly 7% YTD.

As has been the case in the recent months, booming exports (especially of New Electric Vehicles, aka NEVs) led wholesales in September. Domestic sales fared well, too.” Domestic sales of Passenger Vehicles were flat (+0%)YoY, but that was still a good result, as sales a year ago were high due to the post-lock-down rebound. In August, Tesla initiated a new round of price cuts, which triggered a wave of massive price reductions among other major automakers. That, along with the recent personal income tax cut, helped sales.”

Elsewhere in Asia

In Japan, sales remain buoyant, but the selling rate slowed to a more sustainable level of 4.5 million units/year in September, after spiking to an exceptionally high 5.4 million units/year in August. Supply continued to catch up, boosting sales. Yet, there are signs that demand is now slowing, in the face of high inflation and falling real wages. Inflation-adjusted real wages fell for the 17th consecutive month in August, impacting consumers’ purchasing power.

The Korean market has started to lose momentum, hit by tighter credit conditions and a slowing economy, as well as the expiry of the temporary excise tax cut in June. The September selling rate was 1.64 million units/year, not a bad result, but lackluster. All Korean brands, except Kia, reported a YoY decline in sales in September, although that was due partially to a high base. Sales of Light Commercial Vehicles were particularly weak. BEV sales also failed to sustain strong growth.

South America

Preliminary estimates indicate that Brazilian Light Vehicle sales increased by 3.8% YoY in September, to 187,400. As sales have increased YoY, the selling rate also increased to 2.17 million units/year, up from 2.14 million units/year reported in August. Sales for the country have been slowly declining since peaking at 215, 500 in July, as demand has cooled after the end of the government incentive scheme. Falling sales could also account for the increase in inventory, as the quantity of vehicles in stock grew to 265,800 units in September, up from 244,700 units in August.

In Argentina, Light Vehicle sales are estimated to have decreased by 2.9% YoY in September, to 31,400. LV sales suffered a slowdown on a MoM basis, and the selling rate also declined to 347,000 a year, down from 398,000 units/year in August. This is the lowest the selling rate has been since September 2022. There was a sharp drop in sales of imported models in September, accounting for little more than 20% of total volumes, which likely caused the weak overall performance.

*GlobalData

GlobalData says that “4000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, financial, technology and professional services sectors.” J.D. Power is also part of GlobalData. Inquiries at: customersuccess.automotive@globaldata.com.

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.