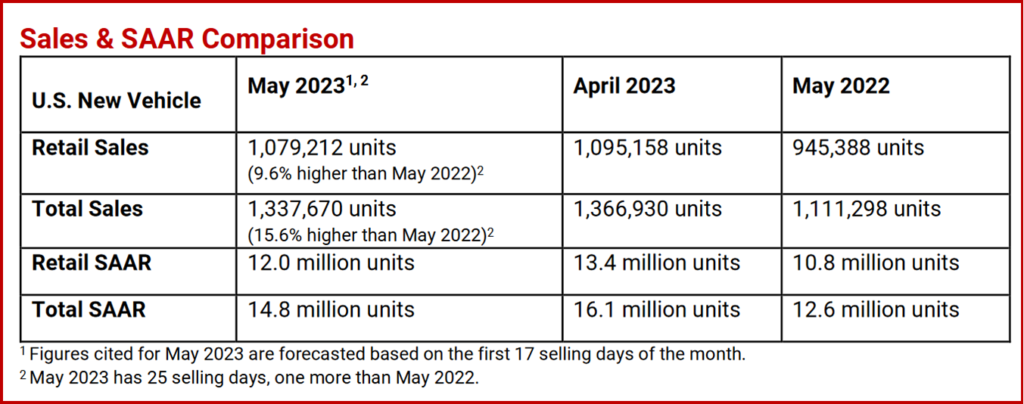

Total US new-vehicle sales for May 2023are projected to reach 1,337,700 units, a 15.6% increase from May 20221, according to a joint forecast from J.D. Power and LMC Automotive* released today. Truck and SUV sales governed the market. May 2023 has 25 selling days, one more than May 2022. Comparing the same sales volume without adjusting for the number of selling days translates to a gain of +20.4% when compared month-over-month with 2022. The Biden Administration’s economic recovery continues to soar upward. The forecast includes both retail and non-retail transactions.2

“The industry is positioned for another strong month in May as retail sales are estimated to surge 9.6% from a year ago. This positive performance is complemented by a projected 0.7% increase in average transaction prices. As a result, it is anticipated that consumers will spend nearly $47 billion on the purchase of new vehicles in May, showcasing a significant 13% growth from a year ago,” said Thomas King, president of the data and analytics division at J.D. Power.

Click for more data.

“Retail inventory levels in May are expected to finish at approximately 1.3 million units, remaining consistent with April’s level. However, this represents a substantial increase of 48% compared with May 2022. The improvement in vehicle availability has led to decreased dealer margins and increased manufacturer incentive spending in that same period. However, both metrics are relatively stable when compared with the previous month. The performance of the retail market continues to demonstrate robust demand for vehicles, augmented by consumers who have delayed purchases due to low inventory,” according to King.

Executive Summary

- The average new-vehicle retail transaction price in May is expected to reach $45,838, a 0.7% increase from May 2022. The previous high for any month at $47,362 was set in December 2022.

- Average incentive spending per unit in May is expected to reach $1788, up from $951 in May 2022. Spending as a percentage of the average MSRP is expected to increase to 3.7%, up 1.6 percentage points from May 2022.

- Average incentive spending per unit on trucks/SUVs in May is expected to be $1,698, up $721 from a year ago, while the average spending on cars is expected to be $1,421, up $567 from a year ago.

- Retail buyers are on pace to spend $46.9 billion on new vehicles, up $5.5 billion from May 2022.

- Truck/SUVs are on pace to account for 79.1% of new-vehicle retail sales in May.

- Fleet sales are expected to total 258,500 units in May, up 49.6% from May 2022 on a selling day adjusted basis. Fleet volume is expected to account for 19% of total light-vehicle sales, up from 15% a year ago.

- Average interest rates for new-vehicle loans are expected to increase to 7.0%, 206 basis points higher than a year ago.

Global Sales Forecast

“The global light-vehicle selling rate hit 85.4 million units in April, up nearly 2 million units from March. Sales volume was up 23.6% year over year to 6.8 million units, as the overall market continues to improve through increased production and less supply disruption. Of the major markets, China led the growth, up 81% from April 2022. Europe (+21.0%), India (+10.6%) and North America (+9.3%) also posted strong results,” said Jeff Schuster, group head and executive vice president, automotive at GlobalData, parent of LMC Automotive.

The seasonally adjusted selling rate (SAAR) in May is expected to decline a tad to 84.5 million units, but significantly above May 2022’s 75.8 million units. Global light-vehicle sales are projected to grow to 7.0 million units, an increase of 12.8% from May 2022. Growth is expected to be more level across the various markets. Eastern Europe is unusual at a nearly 20% increase, as volume returns despite the ongoing war in Ukraine. China is expected to grow 18.5%, followed by North America at 14.7% and Western Europe at 11%.

“April’s volume was in line with expectations, so we are not making any material changes to the topline forecast for 2023. Volume is expected to reach 86.1 million units, up 6.2% from 2022. While risk is balanced overall, there remains some upside potential in 2023 if major markets avoid a recession or consumers show further resilience. There is some mild risk that volume has been pulled forward given expectations for an economic slowdown being delayed until late 2023 or early 2024. The outlook for 2024 global light-vehicle sales is currently holding at 90.3 million units, an increase of 4.9% from 2023,” said Schuster.

*LMC Automotive – a GlobalData Company

LMC Automotive is a leading independent and exclusively automotive focused provider of global forecasting and market intelligence in the areas of vehicle sales, production, powertrains and electrification. The company’s international clients include auto and truck makers, component manufacturers and suppliers, financial and logistics firms, as well as government institutions. LMC Automotive is part of the LMC group, as is J.D. Power. LMC is also the world’s leading economic and business consultancy for the agribusiness sector.

The Global Light Vehicle Sales Forecast published in association with Jato Dynamics Ltd. builds on macro‐economic forecasts generated by LMC partner, the renowned Oxford Economics, which, combined with an examination of demographics, fiscal and regulatory influences by LMC’s own specialist automotive research team, presents twelve‐year forecasts at a global, regional and country levels for Light Vehicle demand in 137 countries. For more information about LMC Automotive, visit www.lmc-auto.com or contact LMC directly at forecasting@lmc-auto.com.

Inevitable Footnotes

1 Figures cited for May 2023 are forecasted based on the first 17 selling days of the month.

2 May 2023 has 25 selling days, one more than May 2022.

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

May US Light Vehicles Sales Forecast Up 20%

Total US new-vehicle sales for May 2023are projected to reach 1,337,700 units, a 15.6% increase from May 20221, according to a joint forecast from J.D. Power and LMC Automotive* released today. Truck and SUV sales governed the market. May 2023 has 25 selling days, one more than May 2022. Comparing the same sales volume without adjusting for the number of selling days translates to a gain of +20.4% when compared month-over-month with 2022. The Biden Administration’s economic recovery continues to soar upward. The forecast includes both retail and non-retail transactions.2

“The industry is positioned for another strong month in May as retail sales are estimated to surge 9.6% from a year ago. This positive performance is complemented by a projected 0.7% increase in average transaction prices. As a result, it is anticipated that consumers will spend nearly $47 billion on the purchase of new vehicles in May, showcasing a significant 13% growth from a year ago,” said Thomas King, president of the data and analytics division at J.D. Power.

Click for more data.

“Retail inventory levels in May are expected to finish at approximately 1.3 million units, remaining consistent with April’s level. However, this represents a substantial increase of 48% compared with May 2022. The improvement in vehicle availability has led to decreased dealer margins and increased manufacturer incentive spending in that same period. However, both metrics are relatively stable when compared with the previous month. The performance of the retail market continues to demonstrate robust demand for vehicles, augmented by consumers who have delayed purchases due to low inventory,” according to King.

Executive Summary

Global Sales Forecast

“The global light-vehicle selling rate hit 85.4 million units in April, up nearly 2 million units from March. Sales volume was up 23.6% year over year to 6.8 million units, as the overall market continues to improve through increased production and less supply disruption. Of the major markets, China led the growth, up 81% from April 2022. Europe (+21.0%), India (+10.6%) and North America (+9.3%) also posted strong results,” said Jeff Schuster, group head and executive vice president, automotive at GlobalData, parent of LMC Automotive.

The seasonally adjusted selling rate (SAAR) in May is expected to decline a tad to 84.5 million units, but significantly above May 2022’s 75.8 million units. Global light-vehicle sales are projected to grow to 7.0 million units, an increase of 12.8% from May 2022. Growth is expected to be more level across the various markets. Eastern Europe is unusual at a nearly 20% increase, as volume returns despite the ongoing war in Ukraine. China is expected to grow 18.5%, followed by North America at 14.7% and Western Europe at 11%.

“April’s volume was in line with expectations, so we are not making any material changes to the topline forecast for 2023. Volume is expected to reach 86.1 million units, up 6.2% from 2022. While risk is balanced overall, there remains some upside potential in 2023 if major markets avoid a recession or consumers show further resilience. There is some mild risk that volume has been pulled forward given expectations for an economic slowdown being delayed until late 2023 or early 2024. The outlook for 2024 global light-vehicle sales is currently holding at 90.3 million units, an increase of 4.9% from 2023,” said Schuster.

*LMC Automotive – a GlobalData Company

LMC Automotive is a leading independent and exclusively automotive focused provider of global forecasting and market intelligence in the areas of vehicle sales, production, powertrains and electrification. The company’s international clients include auto and truck makers, component manufacturers and suppliers, financial and logistics firms, as well as government institutions. LMC Automotive is part of the LMC group, as is J.D. Power. LMC is also the world’s leading economic and business consultancy for the agribusiness sector.

The Global Light Vehicle Sales Forecast published in association with Jato Dynamics Ltd. builds on macro‐economic forecasts generated by LMC partner, the renowned Oxford Economics, which, combined with an examination of demographics, fiscal and regulatory influences by LMC’s own specialist automotive research team, presents twelve‐year forecasts at a global, regional and country levels for Light Vehicle demand in 137 countries. For more information about LMC Automotive, visit www.lmc-auto.com or contact LMC directly at forecasting@lmc-auto.com.

Inevitable Footnotes

1 Figures cited for May 2023 are forecasted based on the first 17 selling days of the month.

2 May 2023 has 25 selling days, one more than May 2022.

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.