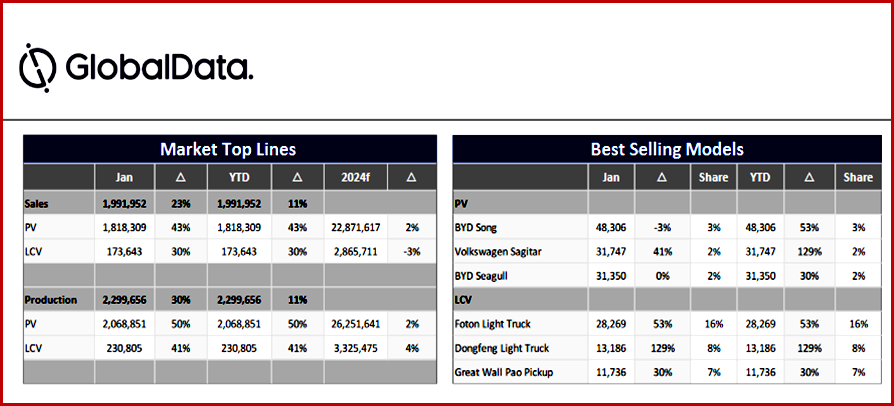

The Chinese auto market soared at the beginning of 2024, according to numbers and an analysis just released by the respected GlobalData* consultancy. Total Light Vehicle (LV) retail sales – wholesales excluding exports – reached 2 million units in January with significant growth of 42% year-on-year (YoY) in the world’s largest auto market. Passenger Vehicle (PV) sales for January increased by 43% YoY to 1.8 million units. Commercial vehicles (CV) achieved growth of 30%, with 173,000 units purchased in January. The month-on-month (MoM) growth rate, saw PVs drop by 25.5%, and CV down 35.2% over the same time.

Looking at mass production, the total LV build in January was 2.3 million units, up 49% YoY. PV production (accounting for 90% of total LV production) in January was 2.1 million units, a YoY increase of 50%. CV production in January was 230, an increase of 41% YoY.

“However, the extremely high YoY increase is related to the low sales base in the same period last year. According to the numbers, the January selling rate was only 19.9 million units/year (a 12-month low), down 24% from 26.2 million units/year in December 2023,” said the Asia-Pacific Light Vehicle Sales Forecasting Team. “Moreover, there were ten more selling days in January 2024 than in the same period in 2023. In January this year, the average daily sales volume was 65.7kunits, almost the same as the 65.2k units seen in January 2023.

Click to enlarge.

“By this measure, domestic sales in January this year were not so strong when compared with January 2023. The main reason for this is that there was a pull-forward of some sales into December, adversely affecting January sales. In addition, at the start of the new year, the price of some car models rebounded, and local consumption incentives and other activities to promote consumption have decreased, all of which have negatively affected sales in January,” said GlobalData.

GlobalData Observations and Commentary

In terms of production, the total LV build in January was 2.3 million units, up 49% YoY. At a vehicle type level, PV production (accounting for 90% of total LV production) in January was 2.1 million units, a YoY increase of 50%. CV production in January was 230,000 units, a rapid increase of 41% YoY.

In January, the YoY trends of joint-venture car companies and Chinese car companies remained quite different. Production by Chinese OEMs grew by 63.9% YoY while output of JV brands increased by 30.8% YoY.

In January, Chinese PV exports reached 364,000 units, a YoY growth rate of 49% and accounted for 18% of total PV production. Although exports in January decreased compared with the prior month, they were still the highest during the same period in history.

Compared with the low growth in automobile exports seen in other countries, China’s automobile exports have boomed. Starting from 2021, vehicle exports have grown strongly. Passenger car exports increased by 114% YoY in 2021 and 56% YoY in 2022. In 2023, the full-year export volume exceeded 4 million units, a YoY increase of 64%, surpassing Japan and setting a new record.

At present, the huge overseas market potential has prompted more and more Chinese car companies to seek to build factories overseas to further reduce costs. Even so, based on conservative estimates of current trends, China’s annual export volume of light vehicles will exceed 5 million units in the next 2-3 years.

From the point of view of new energy vehicles (NEV includes any type of electrification), NEV volume declined 32% compared with December2023, the peak volume of the whole of last year. But when compared with January 2023, NEV sales increased by 85%. At the end of last year, Aito launched its M7 and M9 models, attracting much consumer interest. Their intelligent driving systems will change the market dynamics this year and may speed up the development of the intelligent driving sector overall.

Another interesting development is the EREV (Extended Range Electric Vehicle) segment. Chery unveiled the price of its iCar EREV and the cost is much lower than expected – it will provide the next growth spurt for the EREV segment. However, with the rapid growth of local OEMs, joint ventures appear to have slowed the development of NEVs and reverted to ICE, which is not a good signal for the market.

The penetration rate of NEVs increased to 36% in January. The Dual Credit Policy Version 3.0 together with various NEV incentives may further strengthen NEV growth in 2024 and beyond. In February & March, NEV PV production is expected to reach 682,000 (27%) units and 974,000 (49%) units respectively.

In China, with the recent intensive introduction of a series of macro-control policies and measures, enterprises’ confidence in market development has been further enhanced, production demand has recovered synchronously, and major car companies are also regularly launching new products, further helping to release market demand.

And so, we believe that in the next few years, China’s automobile industry will achieve steady growth, increasingly driven by the rise in exports and demand for NEVs. China’s sales volume reporting has long been based on wholesale numbers as the data source, which includes exports, and our production forecast is driven by sales volume.

GlobalData’s Methodology Change

Because of the strong surge in China’s vehicle exports in recent years, it is becoming necessary to show the constituent elements of the wholesale figures individually to better track domestic demand in China. Starting from January 2024 we have removed export volumes from the wholesales sales data (reported by the China Association of Automobile Manufacturers (CAAM) and now make forecasts based on domestic sales data. On the production side, the current forecast will not be driven by the wholesales forecast alone, but by data sets, one part being the domestic sales forecast, and the other part being the export forecast.

“As we have extensively analyzed the export data and incorporated manufacturers’ plans, we have raised our China production forecast. Specifically, we have raised the forecast by 110k units in 2024, 450k units in 2025, and 400k units in 2026.China’s short- to medium-term production will be driven by export growth. The domestic market is getting saturated, and growth will further slow after NEV tax cuts start phasing out in 2025 and completely stop in 2027,” GlobalData said.

AutoInformed on

*GlobalData

GlobalData says that “4000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, financial, technology and professional services sectors.” J.D. Power is also part of GlobalData. Inquiries at: customersuccess.automotive@globaldata.com

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

Chinese Auto Market is Flying High – Exports a Threat

The Chinese auto market soared at the beginning of 2024, according to numbers and an analysis just released by the respected GlobalData* consultancy. Total Light Vehicle (LV) retail sales – wholesales excluding exports – reached 2 million units in January with significant growth of 42% year-on-year (YoY) in the world’s largest auto market. Passenger Vehicle (PV) sales for January increased by 43% YoY to 1.8 million units. Commercial vehicles (CV) achieved growth of 30%, with 173,000 units purchased in January. The month-on-month (MoM) growth rate, saw PVs drop by 25.5%, and CV down 35.2% over the same time.

Looking at mass production, the total LV build in January was 2.3 million units, up 49% YoY. PV production (accounting for 90% of total LV production) in January was 2.1 million units, a YoY increase of 50%. CV production in January was 230, an increase of 41% YoY.

“However, the extremely high YoY increase is related to the low sales base in the same period last year. According to the numbers, the January selling rate was only 19.9 million units/year (a 12-month low), down 24% from 26.2 million units/year in December 2023,” said the Asia-Pacific Light Vehicle Sales Forecasting Team. “Moreover, there were ten more selling days in January 2024 than in the same period in 2023. In January this year, the average daily sales volume was 65.7kunits, almost the same as the 65.2k units seen in January 2023.

Click to enlarge.

“By this measure, domestic sales in January this year were not so strong when compared with January 2023. The main reason for this is that there was a pull-forward of some sales into December, adversely affecting January sales. In addition, at the start of the new year, the price of some car models rebounded, and local consumption incentives and other activities to promote consumption have decreased, all of which have negatively affected sales in January,” said GlobalData.

GlobalData Observations and Commentary

In terms of production, the total LV build in January was 2.3 million units, up 49% YoY. At a vehicle type level, PV production (accounting for 90% of total LV production) in January was 2.1 million units, a YoY increase of 50%. CV production in January was 230,000 units, a rapid increase of 41% YoY.

In January, the YoY trends of joint-venture car companies and Chinese car companies remained quite different. Production by Chinese OEMs grew by 63.9% YoY while output of JV brands increased by 30.8% YoY.

In January, Chinese PV exports reached 364,000 units, a YoY growth rate of 49% and accounted for 18% of total PV production. Although exports in January decreased compared with the prior month, they were still the highest during the same period in history.

Compared with the low growth in automobile exports seen in other countries, China’s automobile exports have boomed. Starting from 2021, vehicle exports have grown strongly. Passenger car exports increased by 114% YoY in 2021 and 56% YoY in 2022. In 2023, the full-year export volume exceeded 4 million units, a YoY increase of 64%, surpassing Japan and setting a new record.

At present, the huge overseas market potential has prompted more and more Chinese car companies to seek to build factories overseas to further reduce costs. Even so, based on conservative estimates of current trends, China’s annual export volume of light vehicles will exceed 5 million units in the next 2-3 years.

From the point of view of new energy vehicles (NEV includes any type of electrification), NEV volume declined 32% compared with December2023, the peak volume of the whole of last year. But when compared with January 2023, NEV sales increased by 85%. At the end of last year, Aito launched its M7 and M9 models, attracting much consumer interest. Their intelligent driving systems will change the market dynamics this year and may speed up the development of the intelligent driving sector overall.

Another interesting development is the EREV (Extended Range Electric Vehicle) segment. Chery unveiled the price of its iCar EREV and the cost is much lower than expected – it will provide the next growth spurt for the EREV segment. However, with the rapid growth of local OEMs, joint ventures appear to have slowed the development of NEVs and reverted to ICE, which is not a good signal for the market.

The penetration rate of NEVs increased to 36% in January. The Dual Credit Policy Version 3.0 together with various NEV incentives may further strengthen NEV growth in 2024 and beyond. In February & March, NEV PV production is expected to reach 682,000 (27%) units and 974,000 (49%) units respectively.

In China, with the recent intensive introduction of a series of macro-control policies and measures, enterprises’ confidence in market development has been further enhanced, production demand has recovered synchronously, and major car companies are also regularly launching new products, further helping to release market demand.

And so, we believe that in the next few years, China’s automobile industry will achieve steady growth, increasingly driven by the rise in exports and demand for NEVs. China’s sales volume reporting has long been based on wholesale numbers as the data source, which includes exports, and our production forecast is driven by sales volume.

GlobalData’s Methodology Change

Because of the strong surge in China’s vehicle exports in recent years, it is becoming necessary to show the constituent elements of the wholesale figures individually to better track domestic demand in China. Starting from January 2024 we have removed export volumes from the wholesales sales data (reported by the China Association of Automobile Manufacturers (CAAM) and now make forecasts based on domestic sales data. On the production side, the current forecast will not be driven by the wholesales forecast alone, but by data sets, one part being the domestic sales forecast, and the other part being the export forecast.

“As we have extensively analyzed the export data and incorporated manufacturers’ plans, we have raised our China production forecast. Specifically, we have raised the forecast by 110k units in 2024, 450k units in 2025, and 400k units in 2026.China’s short- to medium-term production will be driven by export growth. The domestic market is getting saturated, and growth will further slow after NEV tax cuts start phasing out in 2025 and completely stop in 2027,” GlobalData said.

AutoInformed on

*GlobalData

GlobalData says that “4000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, financial, technology and professional services sectors.” J.D. Power is also part of GlobalData. Inquiries at: customersuccess.automotive@globaldata.com

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.