Click on Chart to enlarge.

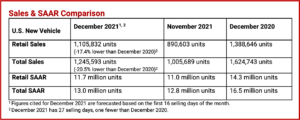

New-vehicle retail sales for December 2021 are forecast to decline when compared with December 2020, according to the latest forecast from J.D. Power and LMC Automotive. Retail sales of new vehicles are expected to reach 1,105,800 units, a -17.4% drop compared with December 2020 when adjusted for selling days. December 2021 has one fewer selling day than December 2020. Comparing the same sales volume without adjusting for the number of selling days translates to a decrease of -20.4% from 2020. New-vehicle retail sales in Q4 2021 are projected to reach 2,923,600 units, a -17.7% decrease from Q4 2020 when adjusted for selling days. New-vehicle retail sales for 2021 are projected to reach 13,074,500 units, a 6.5% increase from 2020 when adjusted for selling days.

Total new-vehicle sales for December 2021, including retail and non-retail transactions, are projected to reach 1,245,600 units, a -20.5% decrease from December 2020. Truck/SUVs are tracking at a record 80.2% of new-vehicle retail sales in December. Comparing the same sales volume without adjusting for the number of selling days translates to a decrease of -23.3% from 2020. The seasonally adjusted annualized rate (SAAR) for total new-vehicle sales is expected to be 13.0 million units, down –3.5 million units from 2020.

- New-vehicle total sales in Q4 2021 are projected to reach 3,302,700 units, a -19.9% decrease from Q4 2020 when adjusted for selling days.

- New-vehicle total sales for 2021 are projected to reach 14,958,900 units, a -4.2% increase from 2020 when adjusted for selling days.

“While the inventory situation has improved modestly since November, supply remains well below the level at which consumer demand for new vehicles can be met. Intense demand with this limited supply is resulting in prices continuing to increase. Average transaction prices are expected to reach a record of $45,743, the first time ever above $45,000 and 20% higher than December 2020 when prices eclipsed $38,000 for the first time,” said Thomas King, president of the data and analytics division at J.D. Power.

“Record transaction prices are partly due to near record-low levels of discounting. The average manufacturer incentive per vehicle is on pace to be a low for the month of December at $1,598, a decrease of $2,291 from a year ago. Expressed as a percentage of the average vehicle MSRP, incentives for December 2021 are trending toward a record-tying low of 3.5%, down nearly 5.5 percentage points from a year ago and the third consecutive month below 4.0%,” King said.

Consumers are projected to spend $50.6 billion on new vehicles this month, the second highest on record for the month of December and the fifth-highest amount for any month on record during the ongoing Biden Administration recovery.

Dealers also benefit from high transaction prices with total retailer profit per unit – inclusive of grosses and finance & insurance income – being on pace to reach a record $5,258, an increase of $3,277 from a year ago and a third consecutive month above $5,000. The gains in per-unit profit more than offset the drop in sales volume, which will make December 2021 the most profitable month on record for retailers. Total aggregate retailer profit from new-vehicle sales is projected to be up 254% from December 2019, reaching $5.8 billion, the first time over $5 billion, Power said.

Record new-vehicle prices are being supported by strong used-vehicle prices, as new-vehicle buyers benefit from more equity on their trade-in vehicles. The average trade-in equity for December is trending towards $10,199, an 83% increase of $4,623 from a year ago and the first time above $10,000. Also, interest rates are favorable when compared with a year ago. The average interest rate for loans in December is expected to decrease nine basis points to 4.05%. Even with lower interest rates and increased trade-in values, the average monthly finance payment is on pace to hit a record high of $680, up $78 from December 2020.

Executive Summary

- The average new-vehicle retail transaction price in December is expected to reach $45,743. The previous high for any month, $44,515, was set in November 2021.

- Average incentive spending per unit in December is expected to reach $1,598, down from $3,889 in December 2020. Spending as a percentage of the average MSRP is expected to fall to 3.5%, down -5.5 percentage points from December 2020.

- Average incentive spending per unit on trucks/SUVs in December is expected to be $1,607, down -$2,291 from a year ago, while the average spending on cars is expected to be $1,562, also down -$2,291 from a year ago.

- Buyers are on pace to spend $50.6 billion on new vehicles, down $2.3 billion from December 2020.

- Truck/SUVs are on pace to account for a record 80.2% of new-vehicle retail sales in December.

- Fleet sales are expected to total 140,000 units in December, down -38.6% from December 2020 on a selling day adjusted basis. Fleet volume is expected to account for 11% of total light-vehicle sales, down from -15% a year ago.

Global Sales Outlook

“Global light-vehicle sales declined -11% year over year in November to 6.7 million units, but the selling rate hit 80.1 million units, the second consecutive month with improvement. November’s rate was up 3.2 million units from October, but still more than 11 million units below the pace of last November.,” said Jeff Schuster, president, Americas operations and global vehicle forecasts, LMC Automotive. China continues to outpace the rest of the world, posting a decline of -8%, while Europe was down -17%. The United States, Japan and South Korea each posted declines near 1-6%. December is projected to maintain a selling rate of 80 million units, with volume off -13% from December 2020.

“A mild improvement in the chip shortage may be overshadowed by risk from the surge in Omicron variant COVID-19 cases. While vehicle shortage and the inventory crunch appear to have peaked, they continue to have a negative effect on demand. The uncertainty of potential restrictions and lockdowns in Europe and Asia could be problematic for global sales levels as we enter 2022. However, 2021 is now expected to finish at just above 81 million units, an increase of 4% from 2020, thanks to a recent increase in China and improvements in some markets in Western Europe. Even with the added risk, the outlook for 2022 has improved to 86 million units, an increase of 750,000 units from last month. We remain cautiously optimistic about the pace of recovery during the next 18 months,” LMC said.

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

December US Auto Sales Forecast – Lower Volume with Record Prices, Profits

Click on Chart to enlarge.

New-vehicle retail sales for December 2021 are forecast to decline when compared with December 2020, according to the latest forecast from J.D. Power and LMC Automotive. Retail sales of new vehicles are expected to reach 1,105,800 units, a -17.4% drop compared with December 2020 when adjusted for selling days. December 2021 has one fewer selling day than December 2020. Comparing the same sales volume without adjusting for the number of selling days translates to a decrease of -20.4% from 2020. New-vehicle retail sales in Q4 2021 are projected to reach 2,923,600 units, a -17.7% decrease from Q4 2020 when adjusted for selling days. New-vehicle retail sales for 2021 are projected to reach 13,074,500 units, a 6.5% increase from 2020 when adjusted for selling days.

Total new-vehicle sales for December 2021, including retail and non-retail transactions, are projected to reach 1,245,600 units, a -20.5% decrease from December 2020. Truck/SUVs are tracking at a record 80.2% of new-vehicle retail sales in December. Comparing the same sales volume without adjusting for the number of selling days translates to a decrease of -23.3% from 2020. The seasonally adjusted annualized rate (SAAR) for total new-vehicle sales is expected to be 13.0 million units, down –3.5 million units from 2020.

“While the inventory situation has improved modestly since November, supply remains well below the level at which consumer demand for new vehicles can be met. Intense demand with this limited supply is resulting in prices continuing to increase. Average transaction prices are expected to reach a record of $45,743, the first time ever above $45,000 and 20% higher than December 2020 when prices eclipsed $38,000 for the first time,” said Thomas King, president of the data and analytics division at J.D. Power.

“Record transaction prices are partly due to near record-low levels of discounting. The average manufacturer incentive per vehicle is on pace to be a low for the month of December at $1,598, a decrease of $2,291 from a year ago. Expressed as a percentage of the average vehicle MSRP, incentives for December 2021 are trending toward a record-tying low of 3.5%, down nearly 5.5 percentage points from a year ago and the third consecutive month below 4.0%,” King said.

Consumers are projected to spend $50.6 billion on new vehicles this month, the second highest on record for the month of December and the fifth-highest amount for any month on record during the ongoing Biden Administration recovery.

Dealers also benefit from high transaction prices with total retailer profit per unit – inclusive of grosses and finance & insurance income – being on pace to reach a record $5,258, an increase of $3,277 from a year ago and a third consecutive month above $5,000. The gains in per-unit profit more than offset the drop in sales volume, which will make December 2021 the most profitable month on record for retailers. Total aggregate retailer profit from new-vehicle sales is projected to be up 254% from December 2019, reaching $5.8 billion, the first time over $5 billion, Power said.

Record new-vehicle prices are being supported by strong used-vehicle prices, as new-vehicle buyers benefit from more equity on their trade-in vehicles. The average trade-in equity for December is trending towards $10,199, an 83% increase of $4,623 from a year ago and the first time above $10,000. Also, interest rates are favorable when compared with a year ago. The average interest rate for loans in December is expected to decrease nine basis points to 4.05%. Even with lower interest rates and increased trade-in values, the average monthly finance payment is on pace to hit a record high of $680, up $78 from December 2020.

Executive Summary

Global Sales Outlook

“Global light-vehicle sales declined -11% year over year in November to 6.7 million units, but the selling rate hit 80.1 million units, the second consecutive month with improvement. November’s rate was up 3.2 million units from October, but still more than 11 million units below the pace of last November.,” said Jeff Schuster, president, Americas operations and global vehicle forecasts, LMC Automotive. China continues to outpace the rest of the world, posting a decline of -8%, while Europe was down -17%. The United States, Japan and South Korea each posted declines near 1-6%. December is projected to maintain a selling rate of 80 million units, with volume off -13% from December 2020.

“A mild improvement in the chip shortage may be overshadowed by risk from the surge in Omicron variant COVID-19 cases. While vehicle shortage and the inventory crunch appear to have peaked, they continue to have a negative effect on demand. The uncertainty of potential restrictions and lockdowns in Europe and Asia could be problematic for global sales levels as we enter 2022. However, 2021 is now expected to finish at just above 81 million units, an increase of 4% from 2020, thanks to a recent increase in China and improvements in some markets in Western Europe. Even with the added risk, the outlook for 2022 has improved to 86 million units, an increase of 750,000 units from last month. We remain cautiously optimistic about the pace of recovery during the next 18 months,” LMC said.

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.