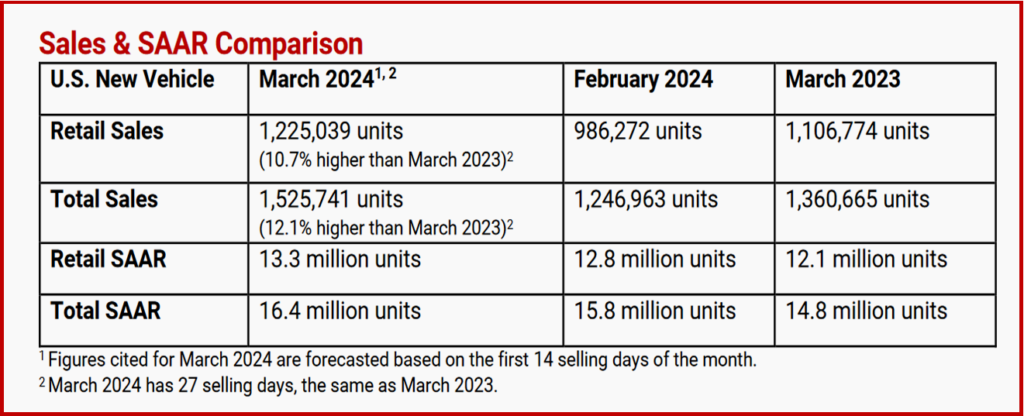

Total US new-vehicle sales for March 2024, are projected to reach 1,525,700 units, a 12.1% increase from March 2023, according to a joint forecast today from J.D. Power and GlobalData.* The seasonally adjusted annualized rate (SAAR) for total new-vehicle sales is expected to be 16.4 million units, up 1.6 million units from March 2023. New-vehicle total sales for Q1 2024 are projected at 3,830,500 units, a 4.5% increase from Q1 2023 when adjusted for selling days as the Biden Administration recovery continues.

New-vehicle retail sales for March 2024 are also expected to increase when compared with March 2023. Retail sales of new vehicles are forecast at 1,225,000 units, a 10.7% increase from March 2023. New-vehicle retail sales for Q1 2024 are projected at 3,066,500 units, a 4.5% increase from Q1 2023 when adjusted for selling days.

Bidenomics is working and so are Americans – working and spending…

“In conjunction with robust sales for Q1, elevated transaction prices mean that consumers are expected to spend more than $129 billion buying new vehicles, an all-time Q1 record. However, while the sales and expenditure performance are impressive, it is coming at the expense of reduced retailer and manufacturer profitability as inventories of unsold vehicles rise and competitive pressures intensify,” said Thomas King, president of the data and analytics division at J.D. Power.

J.D. Power Comments and Data

- Fleet mix is projected at 19.7%, up 1 percentage point from March 2023 and up 18.4% on a volume basis, as several manufacturers increase their focus on fleet sales as a mechanism to address excess inventory.

- The average new-vehicle retail transaction price is declining as manufacturer incentives rise, retailer profit margins fall and availability of lower-priced vehicles increases. Transaction prices are trending towards $44,186, down $1,648 or 3.6%, from March 2023, the largest decline in March ever.

- Consumers are on track to spend nearly $51 billion on new vehicles in March. This is highest ever for the month of March and 6.5% higher than March 2023.

- Total retailer profit per unit (vehicles gross plus finance and insurance income) is expected to be $2487, down 31.9% from March 2023. Rising inventory is the primary factor behind the profit decline and fewer vehicles are selling above the manufacturer’s suggested retail price (MSRP). Thus far in March, only 15.7% of new vehicles have been sold above MSRP, which is down from 31% in March 2023.”

- Total aggregate retailer profit from new-vehicle sales for this month is projected to be $2.9 billion, down 24.8% from March 2023.

- Rising inventory means fewer vehicles are being pre-sold by retailers, with more shoppers able to buy directly off dealer lots. J.D. Power projects that 31.7% of vehicles will sell within 10 days of arriving at the dealership, down from a peak of 58% in March 2022. The average time a new vehicle remains in the dealer’s possession before sale is expected to be 45 days, a 15-day increase from a year ago.

- Manufacturer discounts are expected to rise $170 from a month ago and have materially increased from a year ago. The average incentive spend per vehicle has grown 66.6% from March 2023 and is currently on track to reach $2800. Expressed as a percentage of MSRP, incentive spending is currently at 5.8%, an increase of 2.2 percentage points from a year ago.

- Higher incentive spending is from the increased availability of lease deals, and leasing is growing accordingly. Leasing is expected to account for 24.8% of retail sales, up 5.3 percentage points from 19.6% in March 2023.”

- After rising consistently during the past few years, average monthly loan payments are stabilizing. The average monthly finance payment this month is on pace to be $722, flat from March 2023. The average interest rate for new-vehicle loans is forecast at 6.8%, an increase of 13 basis points from a year ago.

- Thus far in March, average used-vehicle retail prices are $27,950, a -4.3% or $1,248 decrease from a year ago. The decline in used-vehicle values means lower trade-in equity for owners, now trending towards $7558, which is down -$1404 from a year ago.

- With Q1 2024 almost finished, the auto industry is continuing recovery back to pre-pandemic market dynamics. The bias is shifting from low sales volumes/high prices (and profits) to higher sales volumes/lower prices. However, transaction prices and retailer profits remain well above pre-pandemic levels, while manufacturer discounts are well below. This means that, although 2024 will not deliver the record profits observed in recent years, it will likely be the fourth most profitable year on record for retailers. However, rising inventories and rapidly intensifying competition for buyers mean that aggregate industry transaction prices and per unit profitability will likely deteriorate throughout the year.”

More Details at a Glance

- The average new-vehicle retail transaction price in March is expected to reach $44,186, down $1,648 from March 2023. The previous high for any month—$47,329, was set in December 2022.,Average incentive spending per unit in March is expected to reach $2,800, up from $1,680 in March 2023. Spending as a percentage of the average MSRP is expected to increase to 5.8%, up 2.2 percentage points from March 2023.

- Average incentive spending per unit on trucks/SUVs in March is expected to be $2,964, up $1,219 from a year ago, while the average spending on cars is expected to be $2,180, up $750 from a year ago.

- Retail buyers are on pace to spend $51.0 billion on new vehicles, up $3.1 billion from March 2023.

- Trucks/SUVs are will account for 79% of new-vehicle retail sales in March.

- Fleet sales are expected to total 300,702 units in March, up 18.4% from March 2023 on a selling day adjusted basis. Fleet volume is expected to account for 19.7% of total light-vehicle sales, up 1 percentage point from a year ago.

- Average interest rates for new-vehicle loans are expected to increase to 6.8%, 13 basis points higher than a year ago.

EV Outlook

“EV monthly retail share has rebounded from the declines reported in January and February. EV retail share is tracking at 9.1%, almost matching last year’s high of 9.2% in December,” said Elizabeth Krear, vice president, electric vehicle practice at J.D. Power. “Upper-funnel EV shopper interest declined for a fifth consecutive month. New-vehicle shoppers who are ‘very likely’ to consider purchasing an EV for their next vehicle dropped to 22.5%, 1.9 percentage points lower than February. Shoppers continue to cite lack of charging station availability as the top reason for rejecting EVs.

“The EPA final rule that was announced this week relaxes EV adoption requirements for 2027-2030. This not only aligns better with consumer interest in EVs, but also gives the ecosystem more time to ramp up. The EPA rule relaxes EV adoption to 56% by 2032, which is just slightly above our EV baseline forecast for 2032 of 54%. The rule also allows for the opportunity to develop PHEVs and other more fuel-efficient technologies. Interestingly, however, based on the J.D. Power Electric Vehicle Experience (EVX) Ownership Study, satisfaction is lower among owners of PHEVs than owners of full battery electric vehicles,” Krear said.

Global Sales Forecast

“The global light-vehicle selling rate accelerated to 84.6 million units in February, up from 81.5 million in January. [It should be noted that we are now reporting domestic sales in China and excluding Chinese exports that were previously included.] Global sales volume was down 2.8% year over year, although this was heavily influenced by a 24.9% year-over-year decline in China which can be attributed largely to the timing of Lunar New Year celebrations. Japan also saw a 19.1% year-over-year decline in February, although this was probably caused by stoppages in production related to safety testing and certification issues. Other regions performed much more strongly, with U.S. sales expanding 9.2% and Western Europe enjoying growth of 9.4% on the back of improved vehicle availability,” said David Oakley, manager of Americas vehicle sales forecasts at GlobalData.

“Global light-vehicle volume is expected to grow 6.7% year over year in March, while a selling rate of 86.8 million units would represent a modest improvement over February. The United States, China and Europe are projected to see a year-over-year increase in March, although in some markets, the earlier timing of Easter will reduce the number of selling days and keep market activity in check.

“For 2024, we see total light-vehicle sales at 89.3 million units (adjusted for China exports), for a 3.2% increase and up about 200,000 units from our forecast a month ago. A large proportion of the easy gains have now been achieved due to improved inventory levels enabling pent-up demand to be met. In addition, inflation and the cost of living remain challenges facing consumers, while a slowdown in economic growth is still on the cards, even if recent data suggests that the global outlook is improving,” said Oakley.

*GlobalData

GlobalData says that “4000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, financial, technology and professional services sectors.” J.D. Power is also part of GlobalData. Inquiries at: customersuccess.automotive@globaldata.com.

AutoInformed on

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

March US Vehicle Sales Up. Record Q1 Consumer Spending!

Total US new-vehicle sales for March 2024, are projected to reach 1,525,700 units, a 12.1% increase from March 2023, according to a joint forecast today from J.D. Power and GlobalData.* The seasonally adjusted annualized rate (SAAR) for total new-vehicle sales is expected to be 16.4 million units, up 1.6 million units from March 2023. New-vehicle total sales for Q1 2024 are projected at 3,830,500 units, a 4.5% increase from Q1 2023 when adjusted for selling days as the Biden Administration recovery continues.

New-vehicle retail sales for March 2024 are also expected to increase when compared with March 2023. Retail sales of new vehicles are forecast at 1,225,000 units, a 10.7% increase from March 2023. New-vehicle retail sales for Q1 2024 are projected at 3,066,500 units, a 4.5% increase from Q1 2023 when adjusted for selling days.

Bidenomics is working and so are Americans – working and spending…

“In conjunction with robust sales for Q1, elevated transaction prices mean that consumers are expected to spend more than $129 billion buying new vehicles, an all-time Q1 record. However, while the sales and expenditure performance are impressive, it is coming at the expense of reduced retailer and manufacturer profitability as inventories of unsold vehicles rise and competitive pressures intensify,” said Thomas King, president of the data and analytics division at J.D. Power.

J.D. Power Comments and Data

More Details at a Glance

EV Outlook

“EV monthly retail share has rebounded from the declines reported in January and February. EV retail share is tracking at 9.1%, almost matching last year’s high of 9.2% in December,” said Elizabeth Krear, vice president, electric vehicle practice at J.D. Power. “Upper-funnel EV shopper interest declined for a fifth consecutive month. New-vehicle shoppers who are ‘very likely’ to consider purchasing an EV for their next vehicle dropped to 22.5%, 1.9 percentage points lower than February. Shoppers continue to cite lack of charging station availability as the top reason for rejecting EVs.

“The EPA final rule that was announced this week relaxes EV adoption requirements for 2027-2030. This not only aligns better with consumer interest in EVs, but also gives the ecosystem more time to ramp up. The EPA rule relaxes EV adoption to 56% by 2032, which is just slightly above our EV baseline forecast for 2032 of 54%. The rule also allows for the opportunity to develop PHEVs and other more fuel-efficient technologies. Interestingly, however, based on the J.D. Power Electric Vehicle Experience (EVX) Ownership Study, satisfaction is lower among owners of PHEVs than owners of full battery electric vehicles,” Krear said.

Global Sales Forecast

“The global light-vehicle selling rate accelerated to 84.6 million units in February, up from 81.5 million in January. [It should be noted that we are now reporting domestic sales in China and excluding Chinese exports that were previously included.] Global sales volume was down 2.8% year over year, although this was heavily influenced by a 24.9% year-over-year decline in China which can be attributed largely to the timing of Lunar New Year celebrations. Japan also saw a 19.1% year-over-year decline in February, although this was probably caused by stoppages in production related to safety testing and certification issues. Other regions performed much more strongly, with U.S. sales expanding 9.2% and Western Europe enjoying growth of 9.4% on the back of improved vehicle availability,” said David Oakley, manager of Americas vehicle sales forecasts at GlobalData.

“Global light-vehicle volume is expected to grow 6.7% year over year in March, while a selling rate of 86.8 million units would represent a modest improvement over February. The United States, China and Europe are projected to see a year-over-year increase in March, although in some markets, the earlier timing of Easter will reduce the number of selling days and keep market activity in check.

“For 2024, we see total light-vehicle sales at 89.3 million units (adjusted for China exports), for a 3.2% increase and up about 200,000 units from our forecast a month ago. A large proportion of the easy gains have now been achieved due to improved inventory levels enabling pent-up demand to be met. In addition, inflation and the cost of living remain challenges facing consumers, while a slowdown in economic growth is still on the cards, even if recent data suggests that the global outlook is improving,” said Oakley.

*GlobalData

GlobalData says that “4000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, financial, technology and professional services sectors.” J.D. Power is also part of GlobalData. Inquiries at: customersuccess.automotive@globaldata.com.

AutoInformed on

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.