Click for more.

The U.S. economy is at a turning point with the erratic actions of what AutoInformed* observes is the Trump mis-administration threatening our economic health. We are looking at a global trade war leading to a recession or if past Republican economic policies are any indication – a depression. The latest Cox Automotive Industry Forecast** conducted this morning reinforces that view. Brother can you spare a dime?

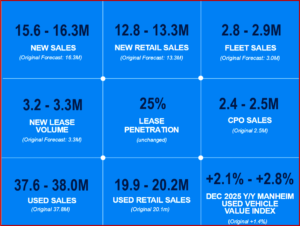

“We are at an interesting crossroads here in late Q one 2025,” said Jonathan Smoke, Chief Economist at Cox. “at the end of last year my wish for you all was that the economy and the auto market would perform to the upside. Today we will be talking about sides, but downward forecasts and darker downsides. The economy and auto market have been relatively strong over the last 6 months. The problem which we will be getting into is that a substantial change in trade through massive increases in tariffs will be highly disruptive to North American vehicle production and could lead to a full scale global trade war and a much weaker the economy. We’re not there yet but we’re a week away from moves that make the dark side more likely,” Smoke said.

“We’ve seen uncertainty grow dramatically over the last two months. And uncertainty can be like a storm that simply ruins the morning commute. If we do see circumstances turned for the negative it will be a squandered opportunity as we were poised for continuing growth. Our quarterly survey of dealer sentiment showed positive momentum at the end of 2024 for dealers views of the market and most importantly dealers views of the future in the 4th quarter optimism post-election.

“First quarter surveys in January and early February saw dealers view of the market and future improve further with optimism at the highest level since the beginning of 2022. Dealers saw sales improving, which is what they expect heading into the spring. The market was perceived as better than last year. Dealers were a little less worried about the economy and most negatives were to clinging concern with interest rates as the number one problem. But those surveys were collected just ahead of the tariff talk getting more intense this month in March.”

“I suspect if we did a poll survey right now. We’d see nervous optimism. The opportunity is still there, but storm clouds are forming on the horizon. We always start these calls with a summary of what we are seeing in the broader economy. That is currently impacting or is likely impacting the auto market in the months to come. We are again involved in the themes we had. Unlike the end of last year when the themes were more positive, the themes are definitely darker now. Instead of a stabilizing economy, we are back to a slowing economy with slowing prospects too. At least we still have growth. According to our forecast and most economists’ forecasts that I survey, the economy is now expected to grow below potential in 2025 because of tariff uncertainty and inflation.

“The worry is that the slowing growth is getting into the territory of an engine stalled becomes more of a risk. The massive policy changes by the administration have been far more aggressive than anyone expected so far. And still the administration has communicated that they are willing to see the economy deteriorate if that is necessary to accomplish their goals.

“While we’re still uncertain about exact policy outcomes, it looks like we are headed for the highest active tariff rate since World War 2 for the auto market. That is especially problematic as such tariffs would be highly disruptive to North American vehicle production – resulting in tighter supply, higher prices and lower production and sales.

“The stock market is down for the year and we will likely see more declines. That produces a negative wealth effect. On spending when the economy and the vehicle market have become more dependent on higher income consumers in recent years. On top of that, rates had declined by more than a full percentage point in the fourth quarter. But have since risen more than that and reached a new 25 year high on the used average rate in February. Affordability has been holding back market potential for years, and between rates and tariffs, affordability looks to get much worse when it had looked like we had turned the corner at the end of last year.

“In addition to tariffs, the auto market also has a substantial amount of EV related policy changes that are likely to unfold later in the year. And the uncertainty from them is especially risky for manufacturers and suppliers trying to adjust their plans it. Feels like uncertainty couldn’t be higher. I’ve narrowed down the list of macro factors to the hard data points that most influenced the. Vehicle market real GDP growth is important for context, but it is the most lagging of the indicators. So it’s not going to help us until it’s much too late. ….

“We are not in a recession or necessarily headed into one. But my optimism about the spring and this year has been shaken. Just think of what the spring could have been had we not been fretting about what comes next? We now know that we have higher tariffs on steel and aluminum and all goods from China.

“The most disruptive move is just one week away, as the postponed 25% tariffs on Canada and Mexico and some amount of reciprocal tariffs will go into effect on April 2nd ( a new definition of April Fool’s or Trump day – AutoCrat) on what the President is calling Liberation Day.

“The tariffs on Mexico and Canada are across the board with no duty drawbacks. As such, if there are no carve outs for autos and parts. They would cause a U.S. -made vehicle to add $3000 in cost and likely $6000 or more on a typical vehicle assembled in Canada or Mexico. If the tariffs go through this time by mid-April, we expect disruption to virtually all North American vehicle production amounting to 20,000 fewer vehicles produced per day. Which is about a 30% hit to production over the longer term. We expect sales of fall, new and used prices to increase and some models to be eliminated. If those tariffs persist – and we’ve yet to hear details about tariffs on the European Union, Japan and South Korea. Just this Monday, the President suggested we’d hear more about auto tariffs before liberation.

“Bottom Line: lower production, tighter supply and higher prices are around the corner. Reminiscent of 2021, uncertainty could make it even worse. Half of the affordable vehicles sold in the US are dependent on Mexico and Canada. With added cost, those nameplates will likely be eliminated. The way this is done also is not conducive to demand increases. Ahead of the change, it’s just been unseen and chaotic. We still don’t know details and we’re days away. Buyers will try and wait for them to go away, but will they go away? On that note, I’ll go take some blood pressure medication,” Smoke said.

*AutoInformed on

- Cox Automotive Alters January Forecast Sales Down

- Cox Automotive – US Vehicle Market Off To Slow Start, But…

**Cox Automotive

Cox Automotive says it is the world’s largest automotive services and technology provider. Fueled by the largest breadth of first-party data fed by 2.3 billion online interactions a year, Cox Automotive tailors leading solutions for car shoppers, automakers, dealers, retailers, lenders, and fleet owners. The company has 25,000-plus employees on five continents and a family of trusted brands that includes Autotrader®, Dealertrack®, Kelley Blue Book®, Manheim®, NextGear Capital™, and vAuto®. Cox Automotive is a subsidiary of Cox Enterprises Inc., a privately owned, Atlanta-based company with $22 billion in annual revenue.

“Americans producing parts for cars assembled in Canada and Mexico are [going to] feel the pain—and there is a risk (a real risk), I think, that U.S. auto buyers go on strike and just don’t buy any cars for a while. Over time, firms will have to move final assembly to the United States—but in the interim, the U.S. market will be under supplied absent (expensive) imports… I should also note that the tariffs on Canada and Mexico are a clear violation of the USMCA,” said the Council for Foreign Relations Senior Fellow Brad W. Setser on X.