Click for more.

The latest light vehicle production forecast out this week by S&P Global Mobility is grim showing declines in every region as original March forecasts that assumed a short Trump Iranian war thought it was a temporary blip. As we said at the time “Well, yes but there is no indication that this will be a short term event or that it’s economic consequences were considered by the whimsical U.S. president who would be king. Moreover the former Detroit Three are heavily dependent on sales of gas-gulping light trucks as fuel prices are climbing with no end in sight. Additionally, the Administration is going it alone in this war, as former allies, who were not informed or consulted, refuse to be drawn into the tragic and increasingly bloody conflict – AutoCrat.”* This brings us to:

“The global auto industry’s near-term outlook is heavily influenced by the ongoing conflict in Iran, with the Strait of Hormuz now expected to remain closed through April, leading to higher oil prices and increased volatility. These conditions are raising manufacturing and logistics costs, putting pressure on vehicle demand and production,” said Mike Wall, Executive Director, Automotive Analysis, S&P Global Mobility yesterday.

“April’s forecast update includes downward revisions across most regions, especially Middle East/Iran and China, as the industry adjusts to persistent geopolitical and macroeconomic challenges. Elevated energy costs, inflation, and supply chain instability are the main factors affecting the industry,” said Wall. “Alternative scenarios, including a severe oil shock, are still being considered due to the risk of extended disruption.”

Regional Highlights by S&P Global Mobility

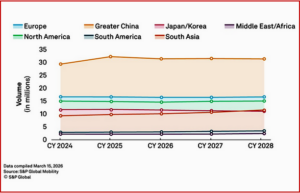

Europe

Europe’s light vehicle production outlook was reduced by 114,000 units for 2026 and 143,000 units for 2027. The forecast reflects additional pressure from the Iran conflict, rising energy costs, and supply chain disruptions, along with ongoing affordability challenges. Demand estimates have been downgraded across key domestic and export markets.

Greater China

Greater China’s light vehicle production outlook was reduced by 239,000 units for 2026 and 156,000 units for 2027. While there was a post-holiday demand recovery in monthly terms, year-on-year performance remains weak due to low consumer confidence and the Iran conflict. Exports remain a growth driver, but structural headwinds like destocking, component pricing and availability, overseas localization, and regulatory tightening led to further downward revisions.

Japan / Korea

The production outlook for Japan was reduced by 60,000 units for 2026 and 26,000 units for 2027, with a long-term reduction of around 94,000 units per year due to sourcing changes. The prolonged Middle East conflict is expected to impact both domestic and export demand through inflation and market instability. South Korea exceeded expectations in March by about 40,000 units, but production forecasts were trimmed by 5,000 units for 2026 and 16,000 units for 2027 due to anticipated weaker demand from higher crude oil prices and ongoing instability.

Middle East / Africa

The production outlook for the Middle East and Africa was reduced by 143,000 units for 2026 and 126,000 units for 2027 but increased by 36,000 units for 2028. The downgrades are mainly due to the Iran conflict, which has disrupted demand, production, logistics, and supply chains, with effects spreading to neighboring Gulf countries. The increase in 2028 is supported by new Chinese automaker production in Egypt and higher light commercial vehicle output in Algeria.

North America

North America’s vehicle production outlook was reduced by 63,000 units for 2026 and 235,000 units for 2027. Near-term builds are still needed to meet demand and rebuild lean inventories, but operational constraints and program transitions, such as General Motors’ full-size pickup retooling and Ford’s F-Series production recovery efforts, remain critical factors. Automakers are expected to maintain output until demand weakening is clear, so a larger downgrade is expected in late 2026 through the first half of 2027.

South America

South America’s production outlook was reduced by 40,000 units for 2026, increased by 5,000 units for 2027, and reduced by 52,000 units for 2028. The near-term downgrade reflects a more cautious stance due to Iran conflict risks, despite strong March results in Brazil driven by discounting, which is not expected to be sustainable. Later-year volumes were also revised down, and Colombia was cut by around 10,000 units per year due to the end of Renault Duster production in 2026 with no immediate successor.

South Asia

South Asia’s production outlook was reduced by 88,000 units for 2026 and 74,000 units for 2027. ASEAN production fell sharply in March, declining 8.5 percent year-on-year to 293,000 units, erasing earlier gains and reflecting the impact of energy-driven inflation and supply chain risks from the Iran conflict. India, highly dependent on Gulf energy imports, saw its forecast reduced by 22,000 units for 2026 and 49,000 units for 2027 as regional uncertainty increases.

*AutoInformed on

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

April 2026 Light Vehicle Production Forecast Drops Globally!

Click for more.

The latest light vehicle production forecast out this week by S&P Global Mobility is grim showing declines in every region as original March forecasts that assumed a short Trump Iranian war thought it was a temporary blip. As we said at the time “Well, yes but there is no indication that this will be a short term event or that it’s economic consequences were considered by the whimsical U.S. president who would be king. Moreover the former Detroit Three are heavily dependent on sales of gas-gulping light trucks as fuel prices are climbing with no end in sight. Additionally, the Administration is going it alone in this war, as former allies, who were not informed or consulted, refuse to be drawn into the tragic and increasingly bloody conflict – AutoCrat.”* This brings us to:

“The global auto industry’s near-term outlook is heavily influenced by the ongoing conflict in Iran, with the Strait of Hormuz now expected to remain closed through April, leading to higher oil prices and increased volatility. These conditions are raising manufacturing and logistics costs, putting pressure on vehicle demand and production,” said Mike Wall, Executive Director, Automotive Analysis, S&P Global Mobility yesterday.

“April’s forecast update includes downward revisions across most regions, especially Middle East/Iran and China, as the industry adjusts to persistent geopolitical and macroeconomic challenges. Elevated energy costs, inflation, and supply chain instability are the main factors affecting the industry,” said Wall. “Alternative scenarios, including a severe oil shock, are still being considered due to the risk of extended disruption.”

Regional Highlights by S&P Global Mobility

Europe

Europe’s light vehicle production outlook was reduced by 114,000 units for 2026 and 143,000 units for 2027. The forecast reflects additional pressure from the Iran conflict, rising energy costs, and supply chain disruptions, along with ongoing affordability challenges. Demand estimates have been downgraded across key domestic and export markets.

Greater China

Greater China’s light vehicle production outlook was reduced by 239,000 units for 2026 and 156,000 units for 2027. While there was a post-holiday demand recovery in monthly terms, year-on-year performance remains weak due to low consumer confidence and the Iran conflict. Exports remain a growth driver, but structural headwinds like destocking, component pricing and availability, overseas localization, and regulatory tightening led to further downward revisions.

Japan / Korea

The production outlook for Japan was reduced by 60,000 units for 2026 and 26,000 units for 2027, with a long-term reduction of around 94,000 units per year due to sourcing changes. The prolonged Middle East conflict is expected to impact both domestic and export demand through inflation and market instability. South Korea exceeded expectations in March by about 40,000 units, but production forecasts were trimmed by 5,000 units for 2026 and 16,000 units for 2027 due to anticipated weaker demand from higher crude oil prices and ongoing instability.

Middle East / Africa

The production outlook for the Middle East and Africa was reduced by 143,000 units for 2026 and 126,000 units for 2027 but increased by 36,000 units for 2028. The downgrades are mainly due to the Iran conflict, which has disrupted demand, production, logistics, and supply chains, with effects spreading to neighboring Gulf countries. The increase in 2028 is supported by new Chinese automaker production in Egypt and higher light commercial vehicle output in Algeria.

North America

North America’s vehicle production outlook was reduced by 63,000 units for 2026 and 235,000 units for 2027. Near-term builds are still needed to meet demand and rebuild lean inventories, but operational constraints and program transitions, such as General Motors’ full-size pickup retooling and Ford’s F-Series production recovery efforts, remain critical factors. Automakers are expected to maintain output until demand weakening is clear, so a larger downgrade is expected in late 2026 through the first half of 2027.

South America

South America’s production outlook was reduced by 40,000 units for 2026, increased by 5,000 units for 2027, and reduced by 52,000 units for 2028. The near-term downgrade reflects a more cautious stance due to Iran conflict risks, despite strong March results in Brazil driven by discounting, which is not expected to be sustainable. Later-year volumes were also revised down, and Colombia was cut by around 10,000 units per year due to the end of Renault Duster production in 2026 with no immediate successor.

South Asia

South Asia’s production outlook was reduced by 88,000 units for 2026 and 74,000 units for 2027. ASEAN production fell sharply in March, declining 8.5 percent year-on-year to 293,000 units, erasing earlier gains and reflecting the impact of energy-driven inflation and supply chain risks from the Iran conflict. India, highly dependent on Gulf energy imports, saw its forecast reduced by 22,000 units for 2026 and 49,000 units for 2027 as regional uncertainty increases.

*AutoInformed on

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.