US Light Vehicle sales totaled 1.06 million units in January, according to the GlobalData* consultancy. The annualized selling rate was 14.8 million units/year in January, down from 16.3 million units/year in December. The daily selling rate was estimated at 42,300 units/day in January, compared with 56,800 units/day in December. According to initial estimates, retail sales totaled around 837,000 units, while fleet sales accounted for approximately ~221,000. This is ~20.9% of total sales. If confirmed by final data, that would be the highest fleet share in 11 months. It is not unusual for fleet sales to account for a larger share of the total market in the opening months of the year, as retail activity slows after the end-of-year push. (AutoInformed.com: January 2024 US Light Vehicle Sales Forecast to Drop a Tad)

“After a flurry of sales activity in December, there was always a risk that January would see some payback, with fewer consumers on the hunt for a new vehicle, and so it transpired. Apart from normal seasonal effects, the current environment is such that buyers remain price-sensitive and if the right deals are not available, volumes are liable to suffer,” said David Oakley, Manager, Americas Sales Forecasts, GlobalData.

Click for more GlobalData.

“Generally speaking, more affordable segments such as Compact Non-Premium SUV, Compact Non-Premium Car and Small Non-Premium SUV performed well in January, but not for every OEM. In addition, cold and wet weather impacted various parts of the country at different times in the month, and this may also have played a role in keeping sales subdued. Traditionally the lowest-volume month of the year, January is often not a good indicator of how the remainder of the year will turn out, and that may prove to be the case again in 2024,” said Oakley.

GlobalData Observations

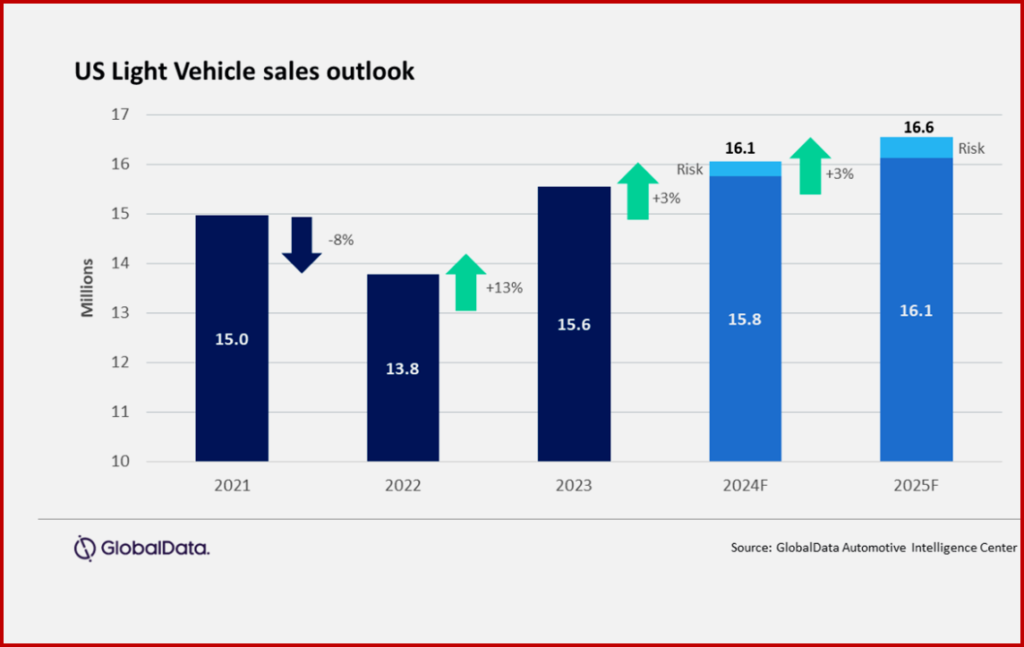

- While weakness at the start of 2024 was expected and it follows a pattern more consistent with a normal seasonal pattern, January ended slightly below expectations. The pattern of sales for the year has been impacted but the forecast for 2024 is holding at 16.1 million units, an increase of 3% from 2023; 2025 is forecast to hold a 3% growth rate as volume climbs to 16.6 million units.

- The payback driven weaker January has driven a surge in days’ supply as the month is expected to have finished at 58 days, up from 42 days in December. While this is the highest level of days’ supply since the pandemic, it is more a function of a pullback in the daily selling rate than a substantial growth in inventory levels. Inventory volume is projected at 2.46 million units, up 5% from December.

- At an OEM level, Toyota Group topped GM by just 600 units to return to the top of the sales rankings, on 166,000 units. Toyota Group and GM have been vying for top spot in recent months, with Toyota having led the market in three out of the last four months, albeit often by small margins. The third largest OEM, Ford Group, enjoyed a relatively strong month, selling 148,000 units, and claiming its highest market share since November 2021. At a brand level, Toyota was once again the market leader, on 143,000 units, but this was only 2000 units ahead of Ford. Chevrolet was a distant third on 109,000 units.

- The Toyota RAV4 was once again the best selling Light Vehicle at 36,300, 5500 units ahead of the Ford F-150.

- Not for the first time in recent months, Compact Non-Premium SUV set a new record high share, at 21.4%, beating the 21.0% share the segment achieved in November 2023. Mid-size Non-Premium SUV was second with a 15.9% share, followed by Large Pickup on 13.2%.

“We continue to expect 2024 to be a return to more normalized patterns of sales and pricing to stabilize, albeit at a higher-than-normal level. Growth in incentives and the eventual cut in interest rates should prove to be a catalyst for continued growth in 2024. There is no question the transition to EVs will be slower than many in the industry expected, but don’t write off EVs in 2024, there will be 47 new BEVs on the market in 2024, accounting for 10% of the total volume. Will this be the year that Tesla’s dominance is finally tested?,” said Jeff Schuster, Vice President Research and Analysis, Automotive at GlobalData.

Global Forecast

Global LV sales finished 2023 strongly, posting a selling rate of 94 million units in December 2023, an increase of 13% from December 2022. Strong domestic and export volume in China, up 24% year over year, once again led the way in increases. 2023 ended at 90 million units, an increase of 11% and the highest level since 2019. While uncertainty will continue to play a leading role for the auto market, a level of stability and more consistency is expected as we start 2024. The forecast for global LV sales in 2024 is for 92.4 million units, a nominal increase of 2% from 2023, but most of the attention may be below the topline. Regulatory pressure remains on the industry for the transition to Electric Vehicles (EVs) and GlobalData expect continued expansion of the EV market in 2024. Battery Electric Vehicles (BEVs) are forecast to account for 15% of global sales in 2024.

*GlobalData

GlobalData says that “4000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, financial, technology and professional services sectors.” J.D. Power is also part of GlobalData. Inquiries at: customersuccess.automotive@globaldata.com

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

Slow Sales Start for US Light Vehicles in January 2024

US Light Vehicle sales totaled 1.06 million units in January, according to the GlobalData* consultancy. The annualized selling rate was 14.8 million units/year in January, down from 16.3 million units/year in December. The daily selling rate was estimated at 42,300 units/day in January, compared with 56,800 units/day in December. According to initial estimates, retail sales totaled around 837,000 units, while fleet sales accounted for approximately ~221,000. This is ~20.9% of total sales. If confirmed by final data, that would be the highest fleet share in 11 months. It is not unusual for fleet sales to account for a larger share of the total market in the opening months of the year, as retail activity slows after the end-of-year push. (AutoInformed.com: January 2024 US Light Vehicle Sales Forecast to Drop a Tad)

“After a flurry of sales activity in December, there was always a risk that January would see some payback, with fewer consumers on the hunt for a new vehicle, and so it transpired. Apart from normal seasonal effects, the current environment is such that buyers remain price-sensitive and if the right deals are not available, volumes are liable to suffer,” said David Oakley, Manager, Americas Sales Forecasts, GlobalData.

Click for more GlobalData.

“Generally speaking, more affordable segments such as Compact Non-Premium SUV, Compact Non-Premium Car and Small Non-Premium SUV performed well in January, but not for every OEM. In addition, cold and wet weather impacted various parts of the country at different times in the month, and this may also have played a role in keeping sales subdued. Traditionally the lowest-volume month of the year, January is often not a good indicator of how the remainder of the year will turn out, and that may prove to be the case again in 2024,” said Oakley.

GlobalData Observations

“We continue to expect 2024 to be a return to more normalized patterns of sales and pricing to stabilize, albeit at a higher-than-normal level. Growth in incentives and the eventual cut in interest rates should prove to be a catalyst for continued growth in 2024. There is no question the transition to EVs will be slower than many in the industry expected, but don’t write off EVs in 2024, there will be 47 new BEVs on the market in 2024, accounting for 10% of the total volume. Will this be the year that Tesla’s dominance is finally tested?,” said Jeff Schuster, Vice President Research and Analysis, Automotive at GlobalData.

Global Forecast

Global LV sales finished 2023 strongly, posting a selling rate of 94 million units in December 2023, an increase of 13% from December 2022. Strong domestic and export volume in China, up 24% year over year, once again led the way in increases. 2023 ended at 90 million units, an increase of 11% and the highest level since 2019. While uncertainty will continue to play a leading role for the auto market, a level of stability and more consistency is expected as we start 2024. The forecast for global LV sales in 2024 is for 92.4 million units, a nominal increase of 2% from 2023, but most of the attention may be below the topline. Regulatory pressure remains on the industry for the transition to Electric Vehicles (EVs) and GlobalData expect continued expansion of the EV market in 2024. Battery Electric Vehicles (BEVs) are forecast to account for 15% of global sales in 2024.

*GlobalData

GlobalData says that “4000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, financial, technology and professional services sectors.” J.D. Power is also part of GlobalData. Inquiries at: customersuccess.automotive@globaldata.com

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.