Cox Automotive* experts on a media call today said U.S. new-vehicle sales in Q1 will increase 5.6% year-over -year (YoY) and reach 3.8 million units. The YoY increase in Q1 sales implies that the new-vehicle market in the U.S. continues to recover slowly from the 10-year low – 13.8 million total sales – recorded in 2022. AutoInformed notes that the Biden Administration recovery continues despite the Federal Reserve’s efforts to harm the economy by keeping interest rates unduly high. Sales volume in March, when announced early in April, is expected to show gains over March 2023 and 2022 as the market continues to expand. The forecast of 1.45 million sales in March would be an increase of 4.5% YoY and close to the 10-year average for the month, historically one of the strongest sales months in a given year. (Read AutoInformed.com on March US Vehicle Sales Up. Record Q1 Consumer Spending!; Cox Automotive – US Vehicle Market Off To Slow Start, But…)

“We have a slowing economy with high interest rates,” said Jonathan Smoke,** Chief Economist at Cox Automotive. “We are seeing the slowing consumer spending. The conundrum is in the details as some metrics like inflation have moved down in the short term, indicating a resilient economy, possibly tipping into reheating. However, other data like retail sales and consumer spending suggest inflation has finally caused consumers to pause on spending.

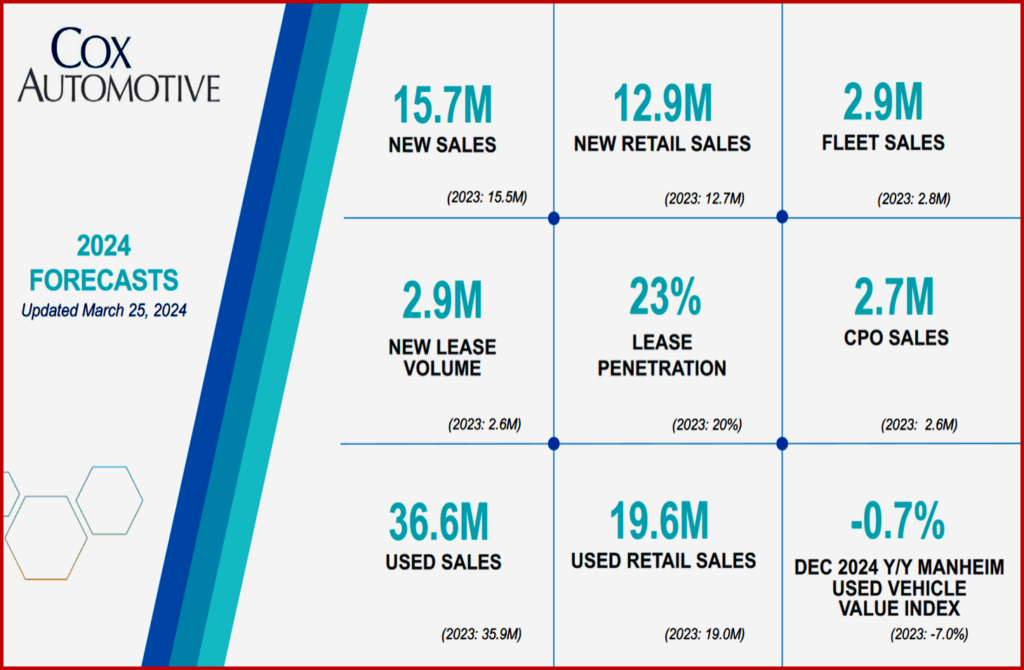

Click for more and to enlarge.

“Meanwhile, the Fed made what sounded like a dovish decision in the last week, reiterating that rates would be cut likely three times before the year end. But not yet. We also in the new vehicle market see a normalizing new vehicle supply and that I would call out as the biggest change in the auto market. This what we saw last year and is likely to continue in 2024. Namely, that new vehicle inventories will continue to build and new vehicle supply will be close to what it was in 2019. Deliveries are growing as production is normalized, but demand appears to be limited, or at least not keeping up. It is not one thing, but several – affordability, what’s possibly satiated pent up demand and growing EV supply,” said Smoke.

The data suggest that healthy sales are being supported by significantly improved new-vehicle inventory levels. At the beginning of March, the total supply of available new vehicles was up more than 50% compared to last March, according to the latest vAuto Live Market View data. The March seasonally adjusted annual rate (SAAR), or selling pace, is expected to finish near 15.5 million, up 0.6 million over last year’s pace but down slightly from February’s surprisingly strong 15.8 million level. This March has 27 sales days, the same as last year but two more than last month. Through Q1, the SAAR is forecast at 15.4 million, up from 15.0 million, or a 2.7% increase, compared to Q1 2023.

EV Grumblings

“Final counts are coming, but the preliminary estimate for Q1 showed 50% year-over-year growth in EV sales,” said Stephanie Valdez Streaty, Director, Industry Insights at Cox. “It is possible the industry will post the first quarter over quarter decline since 2020. However, the numbers show there’s still a EV demand, but market challenges exist – affordability; price, as many EVs still come with a premium price. However, the gap is narrowing. Infrastructure concerns, despite growing charging infrastructure, mean some potential buyers remain wary of EV’s due to perceived limitations and charging availability, reliability and convenience.

“Then there’s market maturity as the EV market matures growth rates slow down as most early adopters already made the transition. Reaching a broader consumer base requires education. engagement and overcoming any additional barriers. Also, there is competition from hybrids. Conventional gas hybrids and plug in hybrids, continue to keep up with the technology transition of this magnitude. [during Q4 of 2023 sales of : HEVs +69%; PHEVs + 49%; BEV +38%] We can expect to see both slowdowns and operations and growth rates. But now let’s get deeper. Dive into the estimated numbers looking at year-over-year for the quarter Q1 is estimated at 15%. However, if you take out Tesla, the growth is 33% in Q1. Tesla’s forecast would only be up 3.2% year-over-year,” said Valdez Streaty.

*Cox Automotive

Cox Automotive says it is the world’s largest automotive services and technology provider. Fueled by the largest breadth of first-party data fed by 2.3 billion online interactions a year, Cox Automotive tailors leading solutions for car shoppers, automakers, dealers, retailers, lenders, and fleet owners. The company has 25,000-plus employees on five continents and a family of trusted brands that includes Autotrader®, Dealertrack®, Kelley Blue Book®, Manheim®, NextGear Capital™, and vAuto®. Cox Automotive is a subsidiary of Cox Enterprises Inc., a privately owned, Atlanta-based company with $22 billion in annual revenue. Visit coxautoinc.com or connect via @CoxAutomotive on X, CoxAutoInc on Facebook, or Cox-Automotive-Inc on LinkedIn.

**Jonathan Smoke – Cox Automotive Chief Economist

Jonathan Smoke leads Cox Automotive’s economic and industry insights team, which tracks key metrics and trends impacting both the wholesale and retail markets for vehicles informed by the proprietary data from the company’s businesses and platforms. For 28 years, Smoke has focused on translating data and trends into relevant actionable insights for the industries that represent the biggest purchases that consumers make in their lifetimes: real estate and automotive. Smoke joined Cox Automotive in 2017.

“Today’s reports show continued progress delivering on President Biden’s agenda to lower costs and grow the economy from the middle out and the bottom up. Consumer sentiment has turned a corner and is up nearly 30% over the last four months, the fastest increase in 30 years. The turnaround in consumer sentiment comes as consumers expect lower inflation and report feeling good about their personal finances. In the second half of 2023, GDP grew faster than any point from 2015 through the pandemic.

“Challenges remain, but working families are starting to see the results of President Biden’s economic plan, with wages rising faster than inflation, record wealth and business creation, and the strongest job market in more than 50 years. We have more work to do to lower costs for American families—building on the progress we’ve made to lower costs for health care, prescription drugs, and housing. With corporate profits still elevated, President Biden will continue to call on companies to pass their savings on to consumers,” – Lael Brainard is National Economic Advisor at the White House.