Click to enlarge.

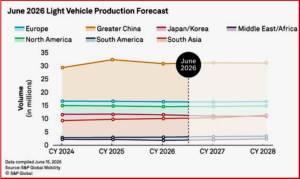

S&P Global Mobility’s May forecast released today noted that Geopolitical risk around the Middle East and the Strait of Hormuz keeps oil risks elevated, with “higher for longer” pricing still a base case and possible shipping/logistics hiccups. The biggest shift is a more constrained outlook for China light-vehicle demand, translating into lower sales and production.

“This domestic weakness in China is partly offset by a stronger export push, as Chinese OEMs redirect volumes to other markets with well-priced, feature-rich products. Elsewhere, most forecast moves are modest, but pressure is building in ASEAN and Middle East/Africa while Europe and North America show more resilience. Overall revisions reflect affordability, energy-cost sensitivity, and accelerating localization/export strategies,” said Mike Wall, Executive Director, Automotive Analysis, S&P Global Mobility.

North America’s production outlook is revised up for both 2026 and 2027, rising by 49,000 and 54,000 units. “Resilience is the key theme, supported by stronger demand and incoming production results, less by forward demand acceleration. Automakers are still expected to build near existing rates, but supply chain/logistics issues and escalating costs remain risks. With US-Iran tensions effectively a stalemate, inflationary pressure could weigh on demand, so production is expected to slow from Q4 2026 through at least Q2 2027 to protect inventories and profitability,” said Wall.

Regional Ruminations

“Europe’s production outlook is stronger for 2026 and 2027, rising by 76,000 and 85,000 units, respectively. Upgrades are led by West & Central Europe (including Turkey), supported by better realized production and notable out-performance from Stellantis and Renault. Tesla is expected to ramp from Q4 2026 as capacity increases, while VW’s MEB ramp is progressing faster than expected. Longer-term momentum is reinforced by affordable compact BEVs and deeper Chinese OEM localization (including Leapmotor and Chery).

“Greater China’s production outlook is cut materially for 2026 and 2027, down 360,000 and 144,000 units. Mainland China demand remains pressured by macro headwinds, weaker discretionary spending, and fading stimulus effects—especially hurting traditional gasoline purchases amid oil-price inflation. NEVs and exports still provide support, but persistent pricing pressure and soft domestic consumption keep the near-term outlook constrained. The market is expected to eventually consolidate further, with stronger players gaining share as weaker manufacturers struggle.

“Japan’s production outlook improves for 2026 (+70,000 units) but eases for 2027 (-12,000 units). Near-term resiliency reflects stronger Q2–Q3 2026 planning despite ongoing Iran war-related risks. However, inflation pressure from higher oil prices remains a key concern. Japan’s longer-term forecast is reduced by about 114,000 units per year, driven by Toyota canceling Lexus ZC and expected Subaru BEV model cancellations. Korea remains under pressure but is downgraded less than feared.

“Middle East/Africa’s production outlook is reduced for 2026 and 2027, down 51,000 and 20,000 units, respectively. The main drivers are a slower ramp-up of new Fiat models, a delay to the new Sandero in Morocco, and partial transfer of Mercedes C-Class production from South Africa to Europe. Recovery is expected later, supported by full-scale new projects in Iran and Morocco. Near-term uncertainty remains elevated given disruption and logistics sensitivity.

“South America sees a mixed revision: 2026 is down 14,000 units, while 2027 rises by 36,000 units. The short-term drop is driven by weaker Brazil exports, especially into Argentina, where Chinese brand sales are accelerating. The 2027 improvement is modest but broad-based across Argentina and Brazil. Argentina benefits from the planned phasing out of an export tax (currently 4.5%) and improving competitiveness abroad, while Brazil’s upgrade reflects increased focus on Chinese brand volumes.

“South Asia’s production outlook is higher in both 2026 and 2027, up 24,000 and 33,000 units. ASEAN output fell 10% y/y in May, and the forecast reflects a deterioration from Middle East conflict effects and Strait of Hormuz disruption, plus weaker domestic demand from macro uncertainty, rising energy costs, and weaker sentiment—driving a 40,000 unit reduction to the 2026 ASEAN forecast. India offsets this with upgrades supported by GST cuts, new launches, and low dealer inventories,” said S&P Global Mobility. [S&P Global Mobility is different from S&P Global Ratings, which is a separately managed division of S&P Global – AutoCrat.]

*AutoInformed on

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn.

He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe.

Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap.

AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks.

Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.

June 2026 Light Vehicle Production Forecast So-So

Click to enlarge.

S&P Global Mobility’s May forecast released today noted that Geopolitical risk around the Middle East and the Strait of Hormuz keeps oil risks elevated, with “higher for longer” pricing still a base case and possible shipping/logistics hiccups. The biggest shift is a more constrained outlook for China light-vehicle demand, translating into lower sales and production.

“This domestic weakness in China is partly offset by a stronger export push, as Chinese OEMs redirect volumes to other markets with well-priced, feature-rich products. Elsewhere, most forecast moves are modest, but pressure is building in ASEAN and Middle East/Africa while Europe and North America show more resilience. Overall revisions reflect affordability, energy-cost sensitivity, and accelerating localization/export strategies,” said Mike Wall, Executive Director, Automotive Analysis, S&P Global Mobility.

North America’s production outlook is revised up for both 2026 and 2027, rising by 49,000 and 54,000 units. “Resilience is the key theme, supported by stronger demand and incoming production results, less by forward demand acceleration. Automakers are still expected to build near existing rates, but supply chain/logistics issues and escalating costs remain risks. With US-Iran tensions effectively a stalemate, inflationary pressure could weigh on demand, so production is expected to slow from Q4 2026 through at least Q2 2027 to protect inventories and profitability,” said Wall.

Regional Ruminations

“Europe’s production outlook is stronger for 2026 and 2027, rising by 76,000 and 85,000 units, respectively. Upgrades are led by West & Central Europe (including Turkey), supported by better realized production and notable out-performance from Stellantis and Renault. Tesla is expected to ramp from Q4 2026 as capacity increases, while VW’s MEB ramp is progressing faster than expected. Longer-term momentum is reinforced by affordable compact BEVs and deeper Chinese OEM localization (including Leapmotor and Chery).

“Greater China’s production outlook is cut materially for 2026 and 2027, down 360,000 and 144,000 units. Mainland China demand remains pressured by macro headwinds, weaker discretionary spending, and fading stimulus effects—especially hurting traditional gasoline purchases amid oil-price inflation. NEVs and exports still provide support, but persistent pricing pressure and soft domestic consumption keep the near-term outlook constrained. The market is expected to eventually consolidate further, with stronger players gaining share as weaker manufacturers struggle.

“Japan’s production outlook improves for 2026 (+70,000 units) but eases for 2027 (-12,000 units). Near-term resiliency reflects stronger Q2–Q3 2026 planning despite ongoing Iran war-related risks. However, inflation pressure from higher oil prices remains a key concern. Japan’s longer-term forecast is reduced by about 114,000 units per year, driven by Toyota canceling Lexus ZC and expected Subaru BEV model cancellations. Korea remains under pressure but is downgraded less than feared.

“Middle East/Africa’s production outlook is reduced for 2026 and 2027, down 51,000 and 20,000 units, respectively. The main drivers are a slower ramp-up of new Fiat models, a delay to the new Sandero in Morocco, and partial transfer of Mercedes C-Class production from South Africa to Europe. Recovery is expected later, supported by full-scale new projects in Iran and Morocco. Near-term uncertainty remains elevated given disruption and logistics sensitivity.

“South America sees a mixed revision: 2026 is down 14,000 units, while 2027 rises by 36,000 units. The short-term drop is driven by weaker Brazil exports, especially into Argentina, where Chinese brand sales are accelerating. The 2027 improvement is modest but broad-based across Argentina and Brazil. Argentina benefits from the planned phasing out of an export tax (currently 4.5%) and improving competitiveness abroad, while Brazil’s upgrade reflects increased focus on Chinese brand volumes.

“South Asia’s production outlook is higher in both 2026 and 2027, up 24,000 and 33,000 units. ASEAN output fell 10% y/y in May, and the forecast reflects a deterioration from Middle East conflict effects and Strait of Hormuz disruption, plus weaker domestic demand from macro uncertainty, rising energy costs, and weaker sentiment—driving a 40,000 unit reduction to the 2026 ASEAN forecast. India offsets this with upgrades supported by GST cuts, new launches, and low dealer inventories,” said S&P Global Mobility. [S&P Global Mobility is different from S&P Global Ratings, which is a separately managed division of S&P Global – AutoCrat.]

*AutoInformed on

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.