Click to enlarge.

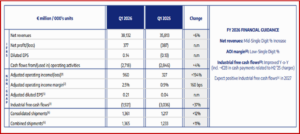

Stellantis N.V. (NYSE: STLA / Euronext Milan: STLAM / Euronext Paris: STLAP) today reported Q1 2026 financial results that show a slight year-over-year improvement.* Net revenues increased 6% year-over-year to €38.1 billion, with improved performance in North America, as well as gains in Enlarged Europe and Middle East & Africa. Net profit increased to €0.4 billion from volume growth and stronger operating performance. As with all global automakers, Stellantis is struggling with trade and tariff wars, as well as the consequences of mid-eastern region military actions. (see footnotes 1 – 10 below)

“As we initiate quarterly reporting, the first three months of 2026 reflect the early results of our actions to return Stellantis to sustainable, profitable growth. The products we launched in 2025 have been well received and we’re confident that the 10 new vehicles planned for 2026 will build on this momentum,” said CEO Antonio Filosa.

Q1 2026 Regional Results

North America: Sales increased 6% versus Q1 2025, with growth of 4% in the U.S., 15% in Canada and 19% in Mexico. Stellantis claimed it outperformed a declining U.S. industry trend which was down 6% in Q1 2026. Market share rose to 7.9%, up 80 basis points year-over-year, driven by Ram, whose U.S. sales increased approximately 20% year-over-year, the highest Q1 since 2023 Jeep also helped with the all-new Jeep® Cherokee, refreshed Jeep® Grand Cherokee, Jeep® Grand Wagoneer and new Dodge Charger SIXPACK now available in dealer showrooms across the U.S.

Enlarged Europe: Sales increased 5% and, including Leapmotor (footnote7), increased 8% versus Q1 2025, driven primarily by Italy, Germany and Spain. Stellantis outperformed the industry’s modest growth in the quarter. EU30 Market share reached 17.5%, up 20 basis points year-over-year and, including Leapmotor (7), 18.1%, up 70 basis points. Growth was said to be helped by a diversified portfolio across BEV, hybrid and ICE powertrains, including the launch of the Fiat Grande Panda ICE on the Smart Car platform. The C-SUV portfolio continues to strengthen, supported by Citroën C5 Aircross and Jeep® Compass. Stellantis reaffirmed its leadership in the EU30 LCV segment, achieving a 28.7% market share.

South America: Sales increased 1% and, including Leapmotor (7), increased 2% versus Q1 2025. Despite a market share decrease of 270 basis points year-over-year, Stellantis maintained its regional leadership with a 21.1% market share, with #1 positions in Brazil at 28.9% market share, and Argentina at 28.9%. Key launches during the quarter included the all-new Ram Dakota, Jeep® Renegade MCA, Jeep® Commander MHEV and Leapmotor B10. Stellantis maintained its leadership in the LCV segment, achieving a 33.8% market share.

Middle East & Africa: Sales remained stable despite a declining industry trend, down 4% year-over-year. Stellantis market share increased to 11.5%, up 50 basis points year-over-year, driven by 18% year-over-year sales growth in Algeria as well as in Türkiye. Key product launches during the quarter included Jeep® Compass and the refreshed Peugeot 408 in Türkiye, as well as the Citroën Basalt in South Africa.

Asia Pacific: Sales declined 4% and, including Leapmotor (7), decreased 2% versus Q1 2025, reflecting a weaker industry environment. Notably, India delivered a 71% sales increase during the quarter, fueled by Citroën’s refreshed line-up.

*AutoInformed on

Inevitable Stellantis Caveats and Footnotes

(1) Adjusted operating income/(loss) excludes from Net profit/(loss) from continuing operations adjustments comprising restructuring and other termination costs, impairments, asset write-offs, disposals of investments and unusual operating income/(expense) that are considered rare or discrete events and are infrequent in nature, as inclusion of such items is not considered to be indicative of the Company’s ongoing operating performance, and also excludes Net financial expenses/(income) and Tax expense/(benefit). Unusual operating income/(expense) are impacts from strategic decisions, as well as events considered rare or discrete and infrequent in nature, as inclusion of such items is not considered to be indicative of the Company’s ongoing operating performance. Unusual operating income/(expense) includes, but may not be limited to impacts from strategic decisions to rationalize Stellantis’ core operations; facility-related costs stemming from Stellantis’ plans to match production capacity and cost structure to market demand, and convergence and integration costs directly related to significant acquisitions or mergers.

(2) Adjusted operating income/(loss) margin is calculated as Adjusted operating income/(loss) divided by Net revenues.

(3) Industrial free cash flows is our key cash flow metric and is calculated as Cash flows from operating activities less: (i) cash flows from operating activities from discontinued operations; (ii) cash flows from operating activities related to financial services, net of eliminations; (iii) investments in property, plant and equipment and intangible assets for industrial activities; (iv) contributions of equity to joint ventures and minor acquisitions of consolidated subsidiaries and equity method and other investments; and adjusted for: (i) net inter-company payments between continuing operations and discontinued operations; (ii) proceeds from disposal of assets and (iii) contributions to defined benefit pension plans, net of tax. The timing of Industrial free cash flows may be affected by the timing of monetization of receivables, factoring and the payment of accounts payables, as well as changes in other components of working capital, which can vary from period to period due to, among other things, cash management initiatives and other factors, some of which may be outside of the Company’s control. In addition, Industrial free cash flows is one of the metrics used in the determination of the annual performance bonus for eligible employees, including members of the senior management.

(4) The majority of our liquidity is available to our treasury operations in Europe and U.S.; however, liquidity is also available to certain subsidiaries which operate in other countries. Cash held in such countries may be subject to restrictions on transfer depending on the foreign jurisdictions in which these subsidiaries operate. Based on our review of such transfer restrictions in the countries in which we operate and maintain material cash balances, (and in particular in Argentina, in which we have €409 million cash and securities at March 31, 2026 (€354 million at December 31, 2025), and in Algeria, in which we have €203 million (€276 million at December 31, 2025)), we do not believe such transfer restrictions had an adverse impact on the Company’s ability to meet its liquidity requirements at the dates presented above. Cash and cash equivalents also include €793 million at March 31, 2026 (€663 million at December 31, 2025) held in bank deposits which are restricted to the operations related to securitization programs and warehouses credit facilities of Stellantis Financial Services U.S.

(5) Adjusted diluted earnings per share (“EPS”) is calculated by adjusting Diluted earnings per share for the post-tax impact per share of the same items excluded from Adjusted operating income as well as tax expense/(benefit) items that are considered rare or infrequent, or whose nature would distort the presentation of the ongoing tax charge of the Company. We believe this non-GAAP measure is useful because it also excludes items that we do not believe are indicative of the Company’s ongoing operating performance and provides investors with a more meaningful comparison of the Company’s ongoing quality of earnings. Adjusted diluted EPS should not be considered as a substitute for Basic earnings per share, Diluted earnings per share from operations or other methods of analyzing our quality of earnings as reported under IFRS.

(6) Combined shipments include shipments by the Company’s consolidated subsidiaries and unconsolidated joint ventures, whereas Consolidated shipments only include shipments by the Company’s consolidated subsidiaries. This includes the vehicles produced by our joint ventures and associates (including Leapmotor International) which are distributed by our consolidated subsidiaries. In addition to the volumes included in consolidated shipments, combined shipments also includes the vehicles distributed by our joint ventures (such as Tofas). Figures by segments may not add up due to rounding.

(7) Leapmotor International is a jointly established Stellantis-controlled company created in 2024, owned 51% by Stellantis and 49% by Leapmotor, to distribute Leapmotor-branded vehicles outside of China. Stellantis does not design, or manufacture Leapmotor-branded vehicles and does not own the Leapmotor brand or intellectual property.

(8) Effective January 2026, the Company’s segment structure was updated to align with how the Chief Operating Decision Maker (“CODM”) reviews performance and allocates resources. Under the revised structure, the CODM reviews the business through the following operating and reportable segments: North America; Enlarged Europe; Middle East & Africa; South America; and Asia Pacific.

The changes in our segment reporting are:

- Maserati is no longer presented as a separate reportable segment as it is managed consistently with the other brands within the regions and are therefore presented on a “where sold” basis). Maserati is therefore no longer presented as a separate reportable segment;

- The Asia Pacific region is now managed as a single operating segment. Previously, the CODM reviewed two operating segments: (i) China and (ii) India & Asia Pacific, which were reported as one reportable segment under IFRS 8. From 2026, these activities are reviewed together, resulting in one operating and reportable segment: Asia Pacific; and

- European used car operations, previously included within Other activities, have been reclassified to the Enlarged Europe segment in line with the CODM’s oversight.

(9) Industrial net financial position is calculated as Debt plus derivative financial liabilities related to industrial activities less (i) cash and cash equivalents, (ii) financial securities that are considered liquid, (iii) current financial receivables from the Company or its jointly controlled financial services entities and (iv) derivative financial assets and collateral deposits. Therefore, debt, cash and cash equivalents and other financial assets/ liabilities pertaining to Stellantis’ financial services entities are excluded from the computation of the Industrial net financial position. Industrial net financial position includes the Industrial net financial position classified as held for sale.

(10) Financial securities are comprised of short term or marketable securities which represent temporary investments but do not satisfy all the requirements to be classified as cash equivalents as they may be subject to risk of change in value (even if they are short-term in nature or marketable.)

Rankings, market share and other industry information are derived from third-party industry sources (e.g., Agence Nationale des Titres Sécurisés (ANTS), Associação Nacional dos Fabricantes de Veículos Automotores (ANFAVEA), Ministry of Infrastructure and Sustainable Mobility (MIMS), S&P Global, Ward’s Automotive) and internal information unless otherwise stated.

For purposes of this document, and unless otherwise stated industry and market share information are for passenger cars (PC) plus light commercial vehicles (LCV), except:

- Enlarged Europe excludes Russia and Belarus;

- Middle East & Africa excludes Iran, Sudan and Syria;

- South America excludes Cuba; and

- Asia Pacific reflects the major markets where Stellantis competes including China (PC only) including licensed sales from Dongfeng Peugeot Citroën Automobiles, Japan (PC), India (PC), South Korea (PC + Pickups), Australia, New Zealand and South East Asia.

Prior period figures have been updated to reflect current information provided by third-party industry sources.

- EU30 = EU 27 (excluding Malta), Iceland, Norway, Switzerland and UK.

- Low emission vehicles (LEV) = battery electric (BEV), plug-in hybrid (PHEV), range-extender electric vehicle (REEV) and fuel cell electric (FCEV) vehicles.

- All Stellantis reported BEV and LEV sales include Citroën Ami, Opel Rocks-e and Fiat Topolino; in countries where these vehicles are classified as quadricycles, they are excluded from Stellantis reported combined sales, industry sales and market share figures.

Stellantis Posts Q1 2026 Net Profit of €0.4 Billion

Click to enlarge.

Stellantis N.V. (NYSE: STLA / Euronext Milan: STLAM / Euronext Paris: STLAP) today reported Q1 2026 financial results that show a slight year-over-year improvement.* Net revenues increased 6% year-over-year to €38.1 billion, with improved performance in North America, as well as gains in Enlarged Europe and Middle East & Africa. Net profit increased to €0.4 billion from volume growth and stronger operating performance. As with all global automakers, Stellantis is struggling with trade and tariff wars, as well as the consequences of mid-eastern region military actions. (see footnotes 1 – 10 below)

“As we initiate quarterly reporting, the first three months of 2026 reflect the early results of our actions to return Stellantis to sustainable, profitable growth. The products we launched in 2025 have been well received and we’re confident that the 10 new vehicles planned for 2026 will build on this momentum,” said CEO Antonio Filosa.

Q1 2026 Regional Results

North America: Sales increased 6% versus Q1 2025, with growth of 4% in the U.S., 15% in Canada and 19% in Mexico. Stellantis claimed it outperformed a declining U.S. industry trend which was down 6% in Q1 2026. Market share rose to 7.9%, up 80 basis points year-over-year, driven by Ram, whose U.S. sales increased approximately 20% year-over-year, the highest Q1 since 2023 Jeep also helped with the all-new Jeep® Cherokee, refreshed Jeep® Grand Cherokee, Jeep® Grand Wagoneer and new Dodge Charger SIXPACK now available in dealer showrooms across the U.S.

Enlarged Europe: Sales increased 5% and, including Leapmotor (footnote7), increased 8% versus Q1 2025, driven primarily by Italy, Germany and Spain. Stellantis outperformed the industry’s modest growth in the quarter. EU30 Market share reached 17.5%, up 20 basis points year-over-year and, including Leapmotor (7), 18.1%, up 70 basis points. Growth was said to be helped by a diversified portfolio across BEV, hybrid and ICE powertrains, including the launch of the Fiat Grande Panda ICE on the Smart Car platform. The C-SUV portfolio continues to strengthen, supported by Citroën C5 Aircross and Jeep® Compass. Stellantis reaffirmed its leadership in the EU30 LCV segment, achieving a 28.7% market share.

South America: Sales increased 1% and, including Leapmotor (7), increased 2% versus Q1 2025. Despite a market share decrease of 270 basis points year-over-year, Stellantis maintained its regional leadership with a 21.1% market share, with #1 positions in Brazil at 28.9% market share, and Argentina at 28.9%. Key launches during the quarter included the all-new Ram Dakota, Jeep® Renegade MCA, Jeep® Commander MHEV and Leapmotor B10. Stellantis maintained its leadership in the LCV segment, achieving a 33.8% market share.

Middle East & Africa: Sales remained stable despite a declining industry trend, down 4% year-over-year. Stellantis market share increased to 11.5%, up 50 basis points year-over-year, driven by 18% year-over-year sales growth in Algeria as well as in Türkiye. Key product launches during the quarter included Jeep® Compass and the refreshed Peugeot 408 in Türkiye, as well as the Citroën Basalt in South Africa.

Asia Pacific: Sales declined 4% and, including Leapmotor (7), decreased 2% versus Q1 2025, reflecting a weaker industry environment. Notably, India delivered a 71% sales increase during the quarter, fueled by Citroën’s refreshed line-up.

*AutoInformed on

Inevitable Stellantis Caveats and Footnotes

(1) Adjusted operating income/(loss) excludes from Net profit/(loss) from continuing operations adjustments comprising restructuring and other termination costs, impairments, asset write-offs, disposals of investments and unusual operating income/(expense) that are considered rare or discrete events and are infrequent in nature, as inclusion of such items is not considered to be indicative of the Company’s ongoing operating performance, and also excludes Net financial expenses/(income) and Tax expense/(benefit). Unusual operating income/(expense) are impacts from strategic decisions, as well as events considered rare or discrete and infrequent in nature, as inclusion of such items is not considered to be indicative of the Company’s ongoing operating performance. Unusual operating income/(expense) includes, but may not be limited to impacts from strategic decisions to rationalize Stellantis’ core operations; facility-related costs stemming from Stellantis’ plans to match production capacity and cost structure to market demand, and convergence and integration costs directly related to significant acquisitions or mergers.

(2) Adjusted operating income/(loss) margin is calculated as Adjusted operating income/(loss) divided by Net revenues.

(3) Industrial free cash flows is our key cash flow metric and is calculated as Cash flows from operating activities less: (i) cash flows from operating activities from discontinued operations; (ii) cash flows from operating activities related to financial services, net of eliminations; (iii) investments in property, plant and equipment and intangible assets for industrial activities; (iv) contributions of equity to joint ventures and minor acquisitions of consolidated subsidiaries and equity method and other investments; and adjusted for: (i) net inter-company payments between continuing operations and discontinued operations; (ii) proceeds from disposal of assets and (iii) contributions to defined benefit pension plans, net of tax. The timing of Industrial free cash flows may be affected by the timing of monetization of receivables, factoring and the payment of accounts payables, as well as changes in other components of working capital, which can vary from period to period due to, among other things, cash management initiatives and other factors, some of which may be outside of the Company’s control. In addition, Industrial free cash flows is one of the metrics used in the determination of the annual performance bonus for eligible employees, including members of the senior management.

(4) The majority of our liquidity is available to our treasury operations in Europe and U.S.; however, liquidity is also available to certain subsidiaries which operate in other countries. Cash held in such countries may be subject to restrictions on transfer depending on the foreign jurisdictions in which these subsidiaries operate. Based on our review of such transfer restrictions in the countries in which we operate and maintain material cash balances, (and in particular in Argentina, in which we have €409 million cash and securities at March 31, 2026 (€354 million at December 31, 2025), and in Algeria, in which we have €203 million (€276 million at December 31, 2025)), we do not believe such transfer restrictions had an adverse impact on the Company’s ability to meet its liquidity requirements at the dates presented above. Cash and cash equivalents also include €793 million at March 31, 2026 (€663 million at December 31, 2025) held in bank deposits which are restricted to the operations related to securitization programs and warehouses credit facilities of Stellantis Financial Services U.S.

(5) Adjusted diluted earnings per share (“EPS”) is calculated by adjusting Diluted earnings per share for the post-tax impact per share of the same items excluded from Adjusted operating income as well as tax expense/(benefit) items that are considered rare or infrequent, or whose nature would distort the presentation of the ongoing tax charge of the Company. We believe this non-GAAP measure is useful because it also excludes items that we do not believe are indicative of the Company’s ongoing operating performance and provides investors with a more meaningful comparison of the Company’s ongoing quality of earnings. Adjusted diluted EPS should not be considered as a substitute for Basic earnings per share, Diluted earnings per share from operations or other methods of analyzing our quality of earnings as reported under IFRS.

(6) Combined shipments include shipments by the Company’s consolidated subsidiaries and unconsolidated joint ventures, whereas Consolidated shipments only include shipments by the Company’s consolidated subsidiaries. This includes the vehicles produced by our joint ventures and associates (including Leapmotor International) which are distributed by our consolidated subsidiaries. In addition to the volumes included in consolidated shipments, combined shipments also includes the vehicles distributed by our joint ventures (such as Tofas). Figures by segments may not add up due to rounding.

(7) Leapmotor International is a jointly established Stellantis-controlled company created in 2024, owned 51% by Stellantis and 49% by Leapmotor, to distribute Leapmotor-branded vehicles outside of China. Stellantis does not design, or manufacture Leapmotor-branded vehicles and does not own the Leapmotor brand or intellectual property.

(8) Effective January 2026, the Company’s segment structure was updated to align with how the Chief Operating Decision Maker (“CODM”) reviews performance and allocates resources. Under the revised structure, the CODM reviews the business through the following operating and reportable segments: North America; Enlarged Europe; Middle East & Africa; South America; and Asia Pacific.

The changes in our segment reporting are:

(9) Industrial net financial position is calculated as Debt plus derivative financial liabilities related to industrial activities less (i) cash and cash equivalents, (ii) financial securities that are considered liquid, (iii) current financial receivables from the Company or its jointly controlled financial services entities and (iv) derivative financial assets and collateral deposits. Therefore, debt, cash and cash equivalents and other financial assets/ liabilities pertaining to Stellantis’ financial services entities are excluded from the computation of the Industrial net financial position. Industrial net financial position includes the Industrial net financial position classified as held for sale.

(10) Financial securities are comprised of short term or marketable securities which represent temporary investments but do not satisfy all the requirements to be classified as cash equivalents as they may be subject to risk of change in value (even if they are short-term in nature or marketable.)

Rankings, market share and other industry information are derived from third-party industry sources (e.g., Agence Nationale des Titres Sécurisés (ANTS), Associação Nacional dos Fabricantes de Veículos Automotores (ANFAVEA), Ministry of Infrastructure and Sustainable Mobility (MIMS), S&P Global, Ward’s Automotive) and internal information unless otherwise stated.

For purposes of this document, and unless otherwise stated industry and market share information are for passenger cars (PC) plus light commercial vehicles (LCV), except:

Prior period figures have been updated to reflect current information provided by third-party industry sources.

About Ken Zino

Ken Zino, editor and publisher of AutoInformed, is a versatile auto industry participant with global experience spanning decades in print and broadcast journalism, as well as social media. He has automobile testing, marketing, public relations and communications experience. He is past president of The International Motor Press Assn, the Detroit Press Club, founding member and first President of the Automotive Press Assn. He is a member of APA, IMPA and the Midwest Automotive Press Assn. He also brings an historical perspective while citing their contemporary relevance of the work of legendary auto writers such as Ken Purdy, Jim Dunne or Jerry Flint, or writers such as Red Smith, Mark Twain, Thomas Jefferson – all to bring perspective to a chaotic automotive universe. Above all, decades after he first drove a car, Zino still revels in the sound of the exhaust as the throttle is blipped during a downshift and the driver’s rush that occurs when the entry, apex and exit points of a turn are smoothly and swiftly crossed. It’s the beginning of a perfect lap. AutoInformed has an editorial philosophy that loves transportation machines of all kinds while promoting critical thinking about the future use of cars and trucks. Zino builds AutoInformed from his background in automotive journalism starting at Hearst Publishing in New York City on Motor and MotorTech Magazines and car testing where he reviewed hundreds of vehicles in his decade-long stint as the Detroit Bureau Chief of Road & Track magazine. Zino has also worked in Europe, and Asia – now the largest automotive market in the world with China at its center.